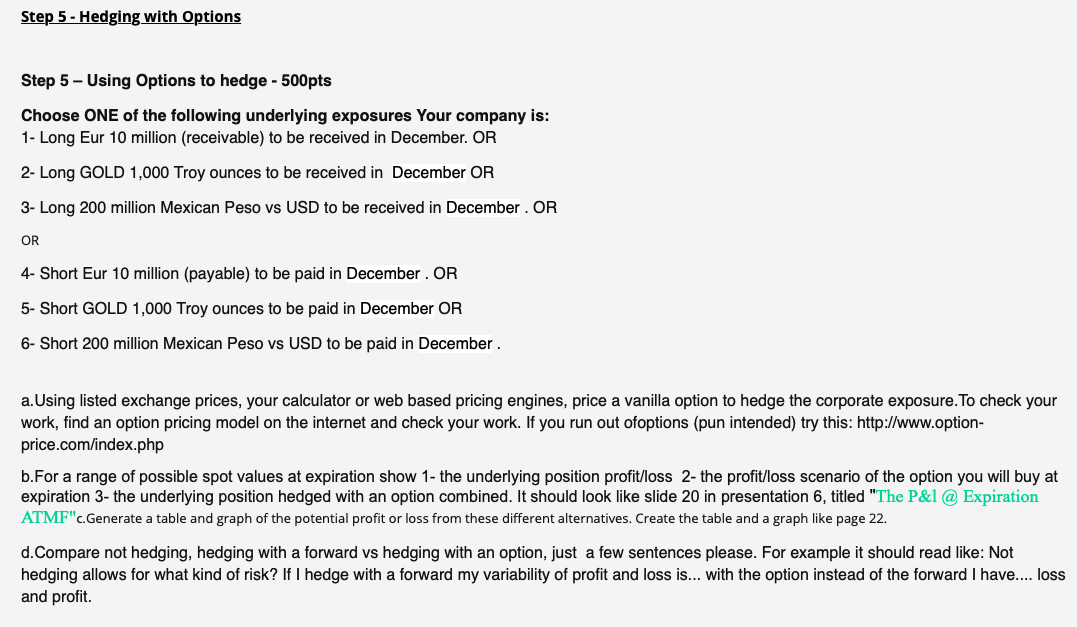

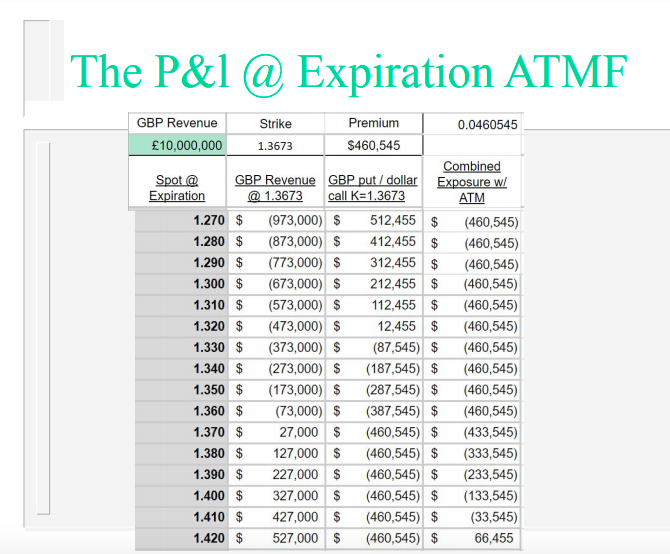

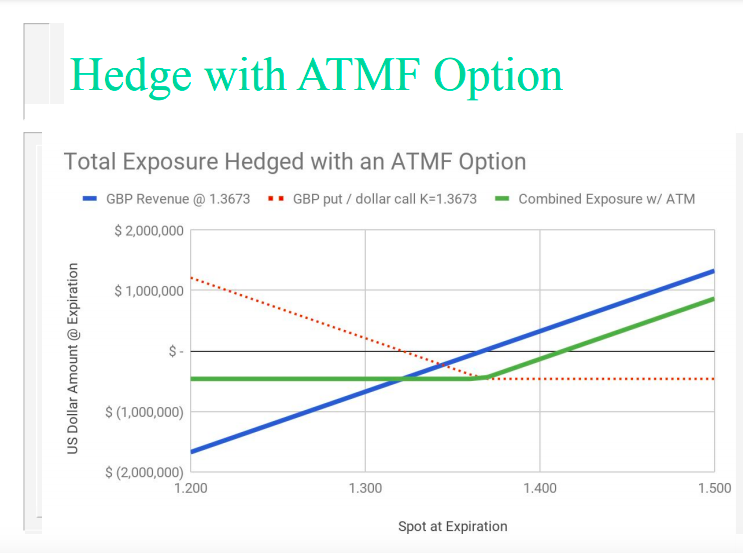

Step 5 - Hedging with Options Step 5 - Using Options to hedge - 500pts Choose ONE of the following underlying exposures Your company is: 1- Long Eur 10 million (receivable) to be received in December. OR 2- Long GOLD 1,000 Troy ounces to be received in December OR 3- Long 200 million Mexican Peso vs USD to be received in December . OR OR 4- Short Eur 10 million (payable) to be paid in December . OR 5- Short GOLD 1,000 Troy ounces to be paid in December OR 6- Short 200 million Mexican Peso vs USD to be paid in December . a.Using listed exchange prices, your calculator or web based pricing engines, price a vanilla option to hedge the corporate exposure. To check your work, find an option pricing model on the internet and check your work. If you run out ofoptions (pun intended) try this: http://www.option- price.com/index.php b.For a range of possible spot values at expiration show 1- the underlying position profit/loss 2- the profit/loss scenario of the option you will buy at expiration 3- the underlying position hedged with an option combined. It should look like slide 20 in presentation 6, titled "The P&l @ Expiration ATMF"c.Generate a table and graph of the potential profit or loss from these different alternatives. Create the table and a graph like page 22. d. Compare not hedging, hedging with a forward vs hedging with an option, just a few sentences please. For example it should read like: Not hedging allows for what kind of risk? If I hedge with a forward my variability of profit and loss is... with the option instead of the forward I have.... loss and profit. The P&l @ Expiration ATMF GBP Revenue Strike Premium 0.0460545 10,000,000 1.3673 $460,545 Combined Spot @ GBP Revenue GBP put / dollar Exposure w/ Expiration @ 1.3673 call K=1.3673 ATM 1.270 $ (973,000) $ 512,455 $ (460,545) 1.280 $ (873,000) $ 412,455 $ (460,545) 1.290 $ (773,000) $ 312,455 $ (460,545) 1.300 $ (673,000) $ 212,455 $ (460,545) 1.310 $ (573,000) $ 112,455 $ (460,545) 1.320 $ (473,000) $ 12,455 $ (460,545) 1.330 $ (373,000) $ (87,545) $ (460,545) 1.340 $ (273,000) $ (187,545) $ (460,545) 1.350 $ (173,000) $ (287,545) $ (460,545) 1.360 $ (73,000) $ (387,545) $ (460,545) 1.370 $ 27,000 $ (460,545) $ (433,545) 1.380 $ 127,000 $ (460,545) $ (333,545) 1.390 $ 227,000 $ (460,545) $ (233,545) 1.400 $ 327,000 $ (460,545) $ (133,545) 1.410 $ 427,000 $ (460,545) $ (33,545) 1.420 $ 527,000 $ (460,545) $ 66,455 Hedge with ATMF Option Total Exposure Hedged with an ATMF Option GBP Revenue @ 1.3673". GBP put / dollar call K=1.3673 - Combined Exposure w/ ATM $ 2,000,000 $ 1,000,000 US Dollar Amount @ Expiration $ $(1,000,000) $ (2,000,000) 1.200 1.300 1.400 1.500 Spot at Expiration Step 5 - Hedging with Options Step 5 - Using Options to hedge - 500pts Choose ONE of the following underlying exposures Your company is: 1- Long Eur 10 million (receivable) to be received in December. OR 2- Long GOLD 1,000 Troy ounces to be received in December OR 3- Long 200 million Mexican Peso vs USD to be received in December . OR OR 4- Short Eur 10 million (payable) to be paid in December . OR 5- Short GOLD 1,000 Troy ounces to be paid in December OR 6- Short 200 million Mexican Peso vs USD to be paid in December . a.Using listed exchange prices, your calculator or web based pricing engines, price a vanilla option to hedge the corporate exposure. To check your work, find an option pricing model on the internet and check your work. If you run out ofoptions (pun intended) try this: http://www.option- price.com/index.php b.For a range of possible spot values at expiration show 1- the underlying position profit/loss 2- the profit/loss scenario of the option you will buy at expiration 3- the underlying position hedged with an option combined. It should look like slide 20 in presentation 6, titled "The P&l @ Expiration ATMF"c.Generate a table and graph of the potential profit or loss from these different alternatives. Create the table and a graph like page 22. d. Compare not hedging, hedging with a forward vs hedging with an option, just a few sentences please. For example it should read like: Not hedging allows for what kind of risk? If I hedge with a forward my variability of profit and loss is... with the option instead of the forward I have.... loss and profit. The P&l @ Expiration ATMF GBP Revenue Strike Premium 0.0460545 10,000,000 1.3673 $460,545 Combined Spot @ GBP Revenue GBP put / dollar Exposure w/ Expiration @ 1.3673 call K=1.3673 ATM 1.270 $ (973,000) $ 512,455 $ (460,545) 1.280 $ (873,000) $ 412,455 $ (460,545) 1.290 $ (773,000) $ 312,455 $ (460,545) 1.300 $ (673,000) $ 212,455 $ (460,545) 1.310 $ (573,000) $ 112,455 $ (460,545) 1.320 $ (473,000) $ 12,455 $ (460,545) 1.330 $ (373,000) $ (87,545) $ (460,545) 1.340 $ (273,000) $ (187,545) $ (460,545) 1.350 $ (173,000) $ (287,545) $ (460,545) 1.360 $ (73,000) $ (387,545) $ (460,545) 1.370 $ 27,000 $ (460,545) $ (433,545) 1.380 $ 127,000 $ (460,545) $ (333,545) 1.390 $ 227,000 $ (460,545) $ (233,545) 1.400 $ 327,000 $ (460,545) $ (133,545) 1.410 $ 427,000 $ (460,545) $ (33,545) 1.420 $ 527,000 $ (460,545) $ 66,455 Hedge with ATMF Option Total Exposure Hedged with an ATMF Option GBP Revenue @ 1.3673". GBP put / dollar call K=1.3673 - Combined Exposure w/ ATM $ 2,000,000 $ 1,000,000 US Dollar Amount @ Expiration $ $(1,000,000) $ (2,000,000) 1.200 1.300 1.400 1.500 Spot at Expiration