Answered step by step

Verified Expert Solution

Question

1 Approved Answer

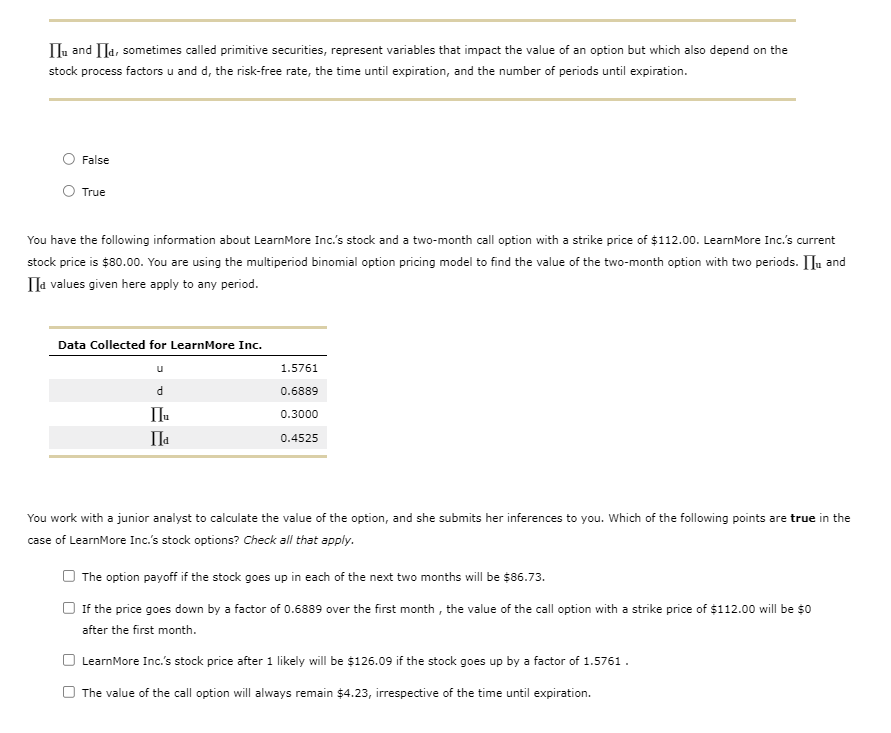

stock process factors u and d, the risk-free rate, the time until expiration, and the number of periods until expiration. False True You have the

stock process factors u and d, the risk-free rate, the time until expiration, and the number of periods until expiration. False True You have the following information about LearnMore Inc.'s stock and a two-month call option with a strike price of $112.00. LearnMore Inc.'s current stock price is $80.00. You are using the multiperiod binomial option pricing model to find the value of the two-month option with two periods. u and d values given here apply to any period. You work with a junior analyst to calculate the value of the option, and she submits her inferences to you. Which of the following points are true in the case of LearnMore Inc.'s stock options? Check all that apply. The option payoff if the stock goes up in each of the next two months will be $86.73. If the price goes down by a factor of 0.6889 over the first month, the value of the call option with a strike price of $112.00 will be $0 after the first month. LearnMore Inc.'s stock price after 1 likely will be $126.09 if the stock goes up by a factor of 1.5761 . The value of the call option will always remain $4.23, irrespective of the time until expiration

stock process factors u and d, the risk-free rate, the time until expiration, and the number of periods until expiration. False True You have the following information about LearnMore Inc.'s stock and a two-month call option with a strike price of $112.00. LearnMore Inc.'s current stock price is $80.00. You are using the multiperiod binomial option pricing model to find the value of the two-month option with two periods. u and d values given here apply to any period. You work with a junior analyst to calculate the value of the option, and she submits her inferences to you. Which of the following points are true in the case of LearnMore Inc.'s stock options? Check all that apply. The option payoff if the stock goes up in each of the next two months will be $86.73. If the price goes down by a factor of 0.6889 over the first month, the value of the call option with a strike price of $112.00 will be $0 after the first month. LearnMore Inc.'s stock price after 1 likely will be $126.09 if the stock goes up by a factor of 1.5761 . The value of the call option will always remain $4.23, irrespective of the time until expiration Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ultimate Beginner S Guide To Real Estate Investment

Authors: Romanj V. Ivanov

1st Edition

979-8865988915