Question: Stock Selection Case Study Markowitz won the Nobel Prize for his work in stock portfolio theory. He was the first to measure portfolio risk using

Stock Selection Case Study

Markowitz won the Nobel Prize for his work in stock portfolio theory. He was

the first to measure portfolio risk using the variance of returns.

introduced stock selection based on an "efficient frontier", namely, by picking

the stocks that give the portfolio "with minimum variance for a given return"

and "maximum return for a given variance."

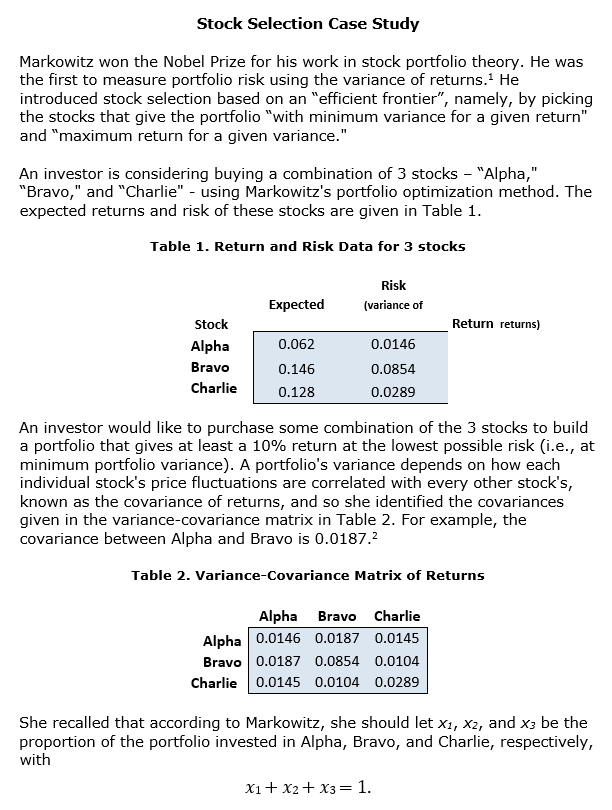

An investor is considering buying a combination of stocks "Alpha,"

"Bravo," and "Charlie" using Markowitz's portfolio optimization method. The

expected returns and risk of these stocks are given in Table

Table Return and Risk Data for stocks

An investor would like to purchase some combination of the stocks to build

a portfolio that gives at least a return at the lowest possible risk ie at

minimum portfolio variance A portfolio's variance depends on how each

individual stock's price fluctuations are correlated with every other stock's,

known as the covariance of returns, and so she identified the covariances

given in the variancecovariance matrix in Table For example, the

covariance between Alpha and Bravo is

Table VarianceCovariance Matrix of Returns

She recalled that according to Markowitz, she should let and be the

proportion of the portfolio invested in Alpha, Bravo, and Charlie, respectively,

with

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock