Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Strike Price is 101.0 5. An investor believes in the liquidity theory and observes the following yield curve: (8 points) Maturity (years) Zero Coupon Yield

Strike Price is 101.0

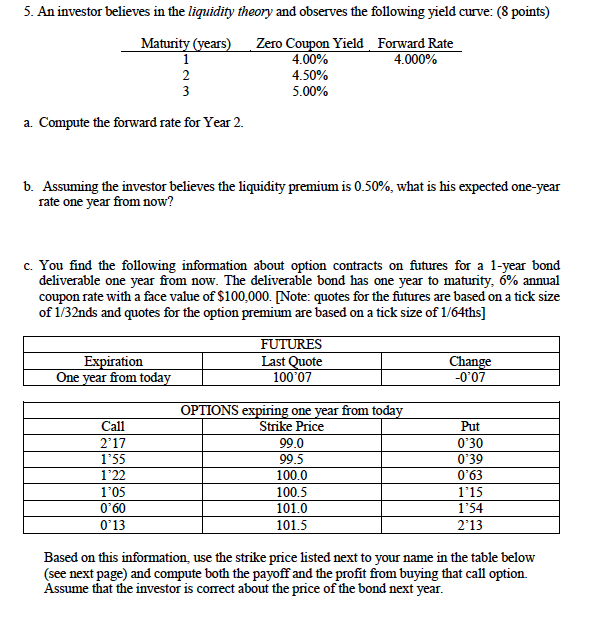

5. An investor believes in the liquidity theory and observes the following yield curve: (8 points) Maturity (years) Zero Coupon Yield Forward Rate 1 4.00% 4.000% 2 4.50% 3 5.00% a. Compute the forward rate for Year 2. b. Assuming the investor believes the liquidity premium is 0.50%, what is his expected one-year rate one year from now? c. You find the following information about option contracts on futures for a 1-year bond deliverable one year from now. The deliverable bond has one year to maturity, 6% annual coupon rate with a face value of $100,000. [Note: quotes for the futures are based on a tick size of 1/32nds and quotes for the option premium are based on a tick size of 1/64ths] Expiration One year from today FUTURES Last Quote 100'07 Change -0'07 Call 2'17 1'55 1'22 1'05 0'60 OPTIONS expiring one year from today Strike Price 99.0 99.5 100.0 100.5 101.0 101.5 Put 0:30 0'39 0'63 1'15 1'54 2'13 0'13 Based on this information, use the strike price listed next to your name in the table below (see next page) and compute both the payoff and the profit from buying that call option Assume that the investor is correct about the price of the bond next year. 5. An investor believes in the liquidity theory and observes the following yield curve: (8 points) Maturity (years) Zero Coupon Yield Forward Rate 1 4.00% 4.000% 2 4.50% 3 5.00% a. Compute the forward rate for Year 2. b. Assuming the investor believes the liquidity premium is 0.50%, what is his expected one-year rate one year from now? c. You find the following information about option contracts on futures for a 1-year bond deliverable one year from now. The deliverable bond has one year to maturity, 6% annual coupon rate with a face value of $100,000. [Note: quotes for the futures are based on a tick size of 1/32nds and quotes for the option premium are based on a tick size of 1/64ths] Expiration One year from today FUTURES Last Quote 100'07 Change -0'07 Call 2'17 1'55 1'22 1'05 0'60 OPTIONS expiring one year from today Strike Price 99.0 99.5 100.0 100.5 101.0 101.5 Put 0:30 0'39 0'63 1'15 1'54 2'13 0'13 Based on this information, use the strike price listed next to your name in the table below (see next page) and compute both the payoff and the profit from buying that call option Assume that the investor is correct about the price of the bond next yearStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Finance Practical Case Studies Volume 2

Authors: Henry A. Davis

2nd Edition

1843740524, 9781843740520