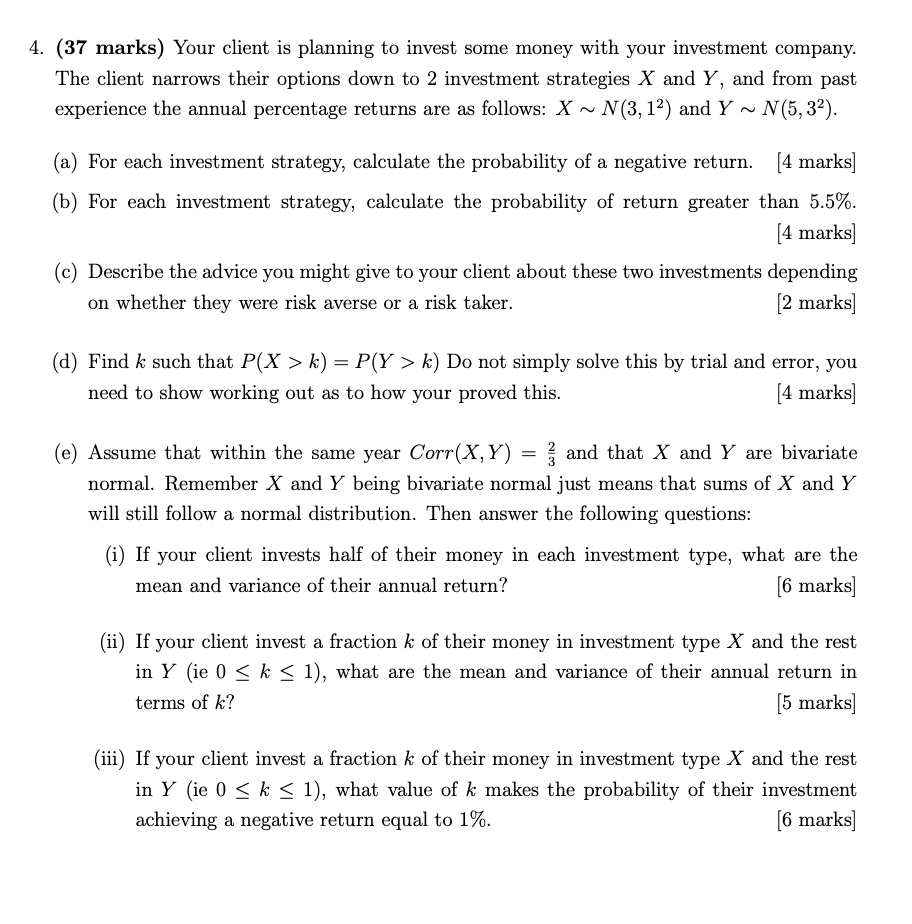

Struggling with part e) sections ii & iii as well as well as part f) in this question. Manage to solve most of the other sections. And could formulas be provided because it helps me understand how the to solve them.

a) 0.0013

b) 0.4338

c) if he is risk averse he souls go for investment X and if he's a risk taker he should go for Y

d) k = 2

e)i) mean is 4 and var is 3.5

ii) ?

iii) ?

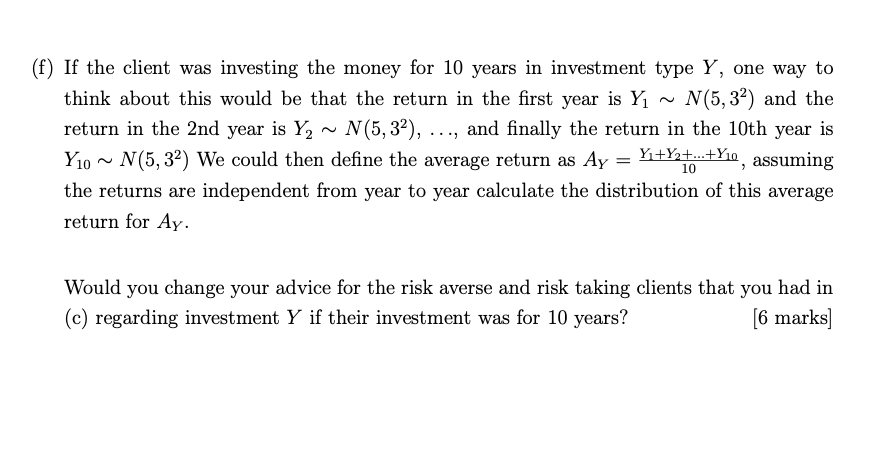

f) ?

4. (37 marks) Your client is planning to invest some money with your investment company. The client narrows their options down to 2 investment strategies X and Y, and from past experience the annual percentage returns are as follows: X ~ N(3, 12) and Y N N(5, 32). (a) For each investment strategy, calculate the probability of a negative return. [4 marks] (b) For each investment strategy, calculate the probability of return greater than 5.5%. [4 marks] (c) Describe the advice you might give to your client about these two investments depending on whether they were risk averse or a risk taker. [2 marks] (d) Find it such that P(X > k) = P(Y > It) Do not simply solve this by trial and error, you need to show working out as to how your preved this. [4 marks] (e) Assume that within the same year Corr(X, Y) = g and that X and Y are bivariate normal. Remember X and Y being bivariate normal just means that sums of X and Y will still follow a normal distribution. Then answer the following questions: (i) If your client invests half of their money in each investment type, what are the mean and variance of their annual return? [6 marks] (ii) If your client invest a fraction k of their money in investment type X and the rest in Y (ie 0 S k S 1), what are the mean and variance of their annual return in terms of k? [5 marks] (iii) If your client invest a fraction k of their money in investment type X and the rest in Y (ie 0 S k g 1), what value of It makes the probability of their investment achieving a negative return equal to 1%. [6 marks] (f) If the client was investing the money for 10 years in investment type Y, one way to think about this would be that the return in the first year is Y1 ~ N(5,32) and the return in the 2nd year is Y2 ~ N(5, 32), ..., and finally the return in the 10th year is Y10 ~ N(5, 32) We could then define the average return as Ay = Withat the, assuming the returns are independent from year to year calculate the distribution of this average return for Ay. Would you change your advice for the risk averse and risk taking clients that you had in (c) regarding investment Y if their investment was for 10 years? [6 marks]