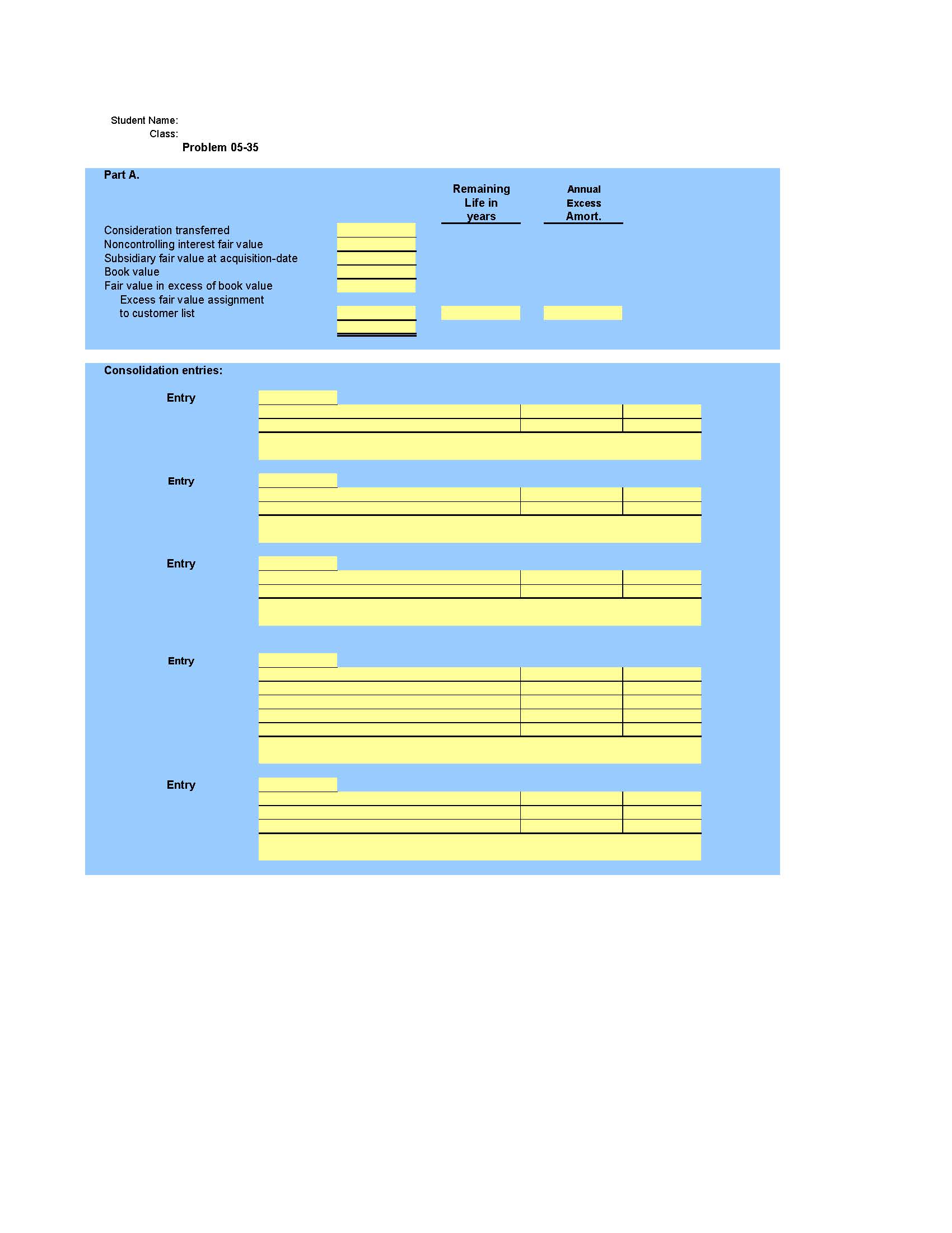

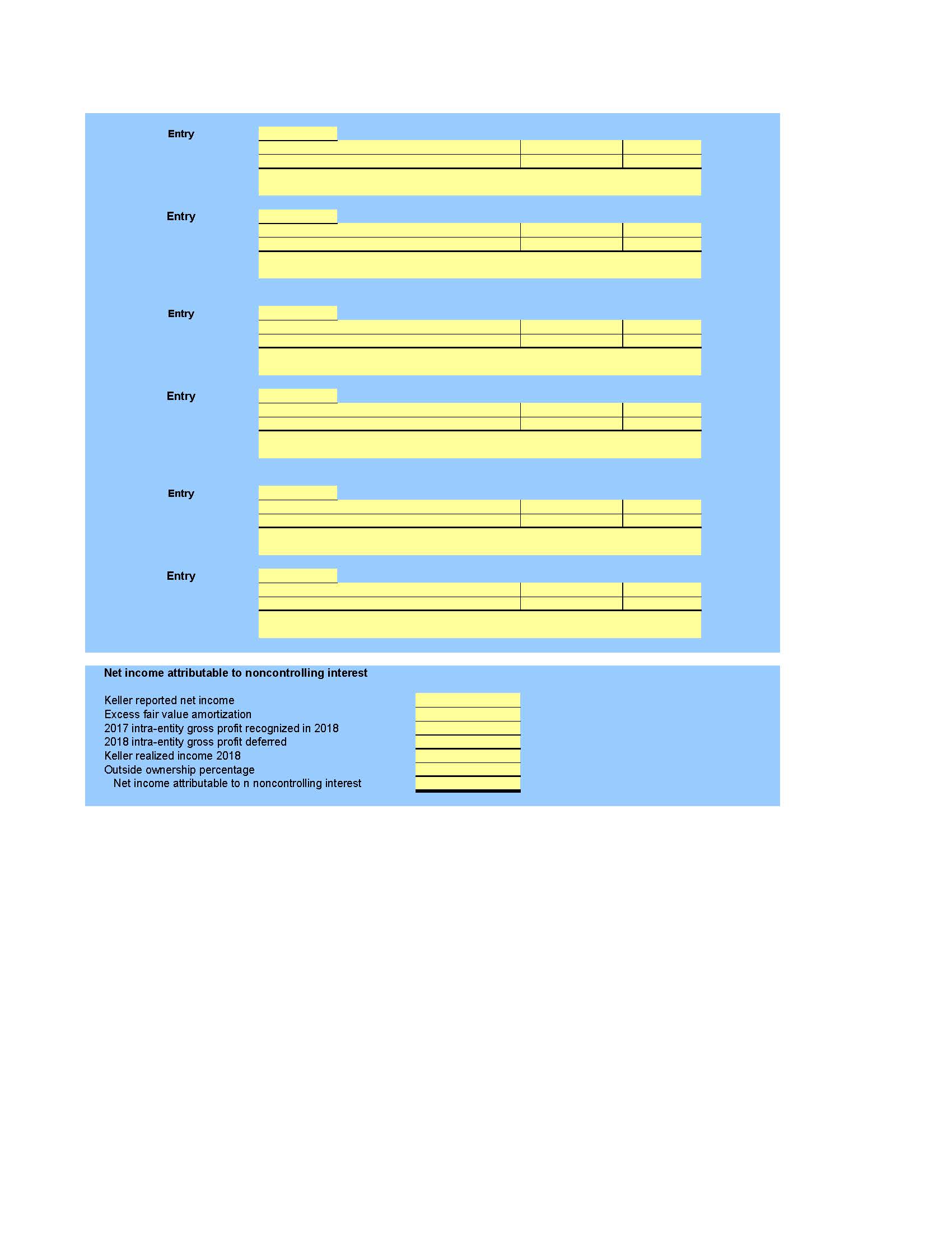

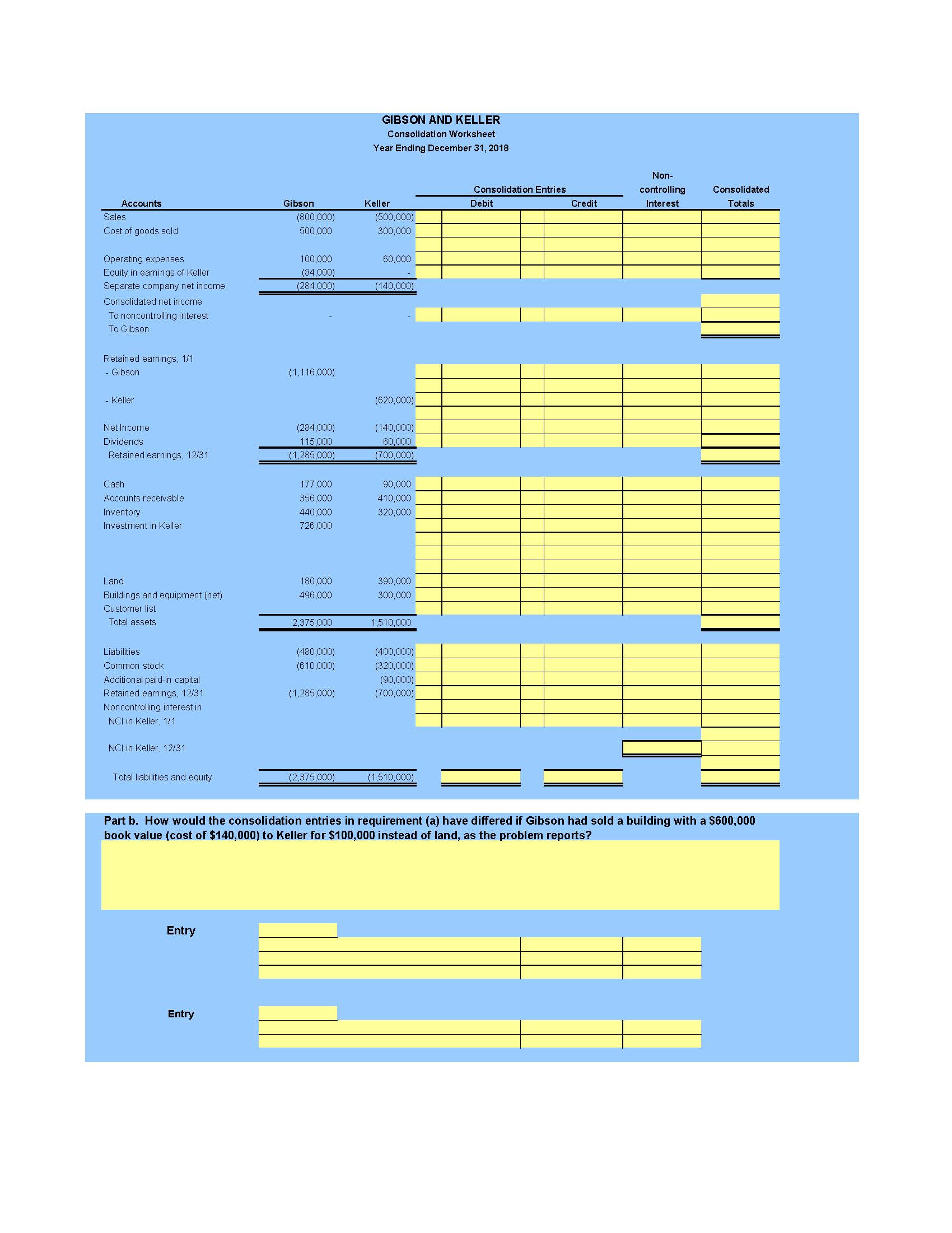

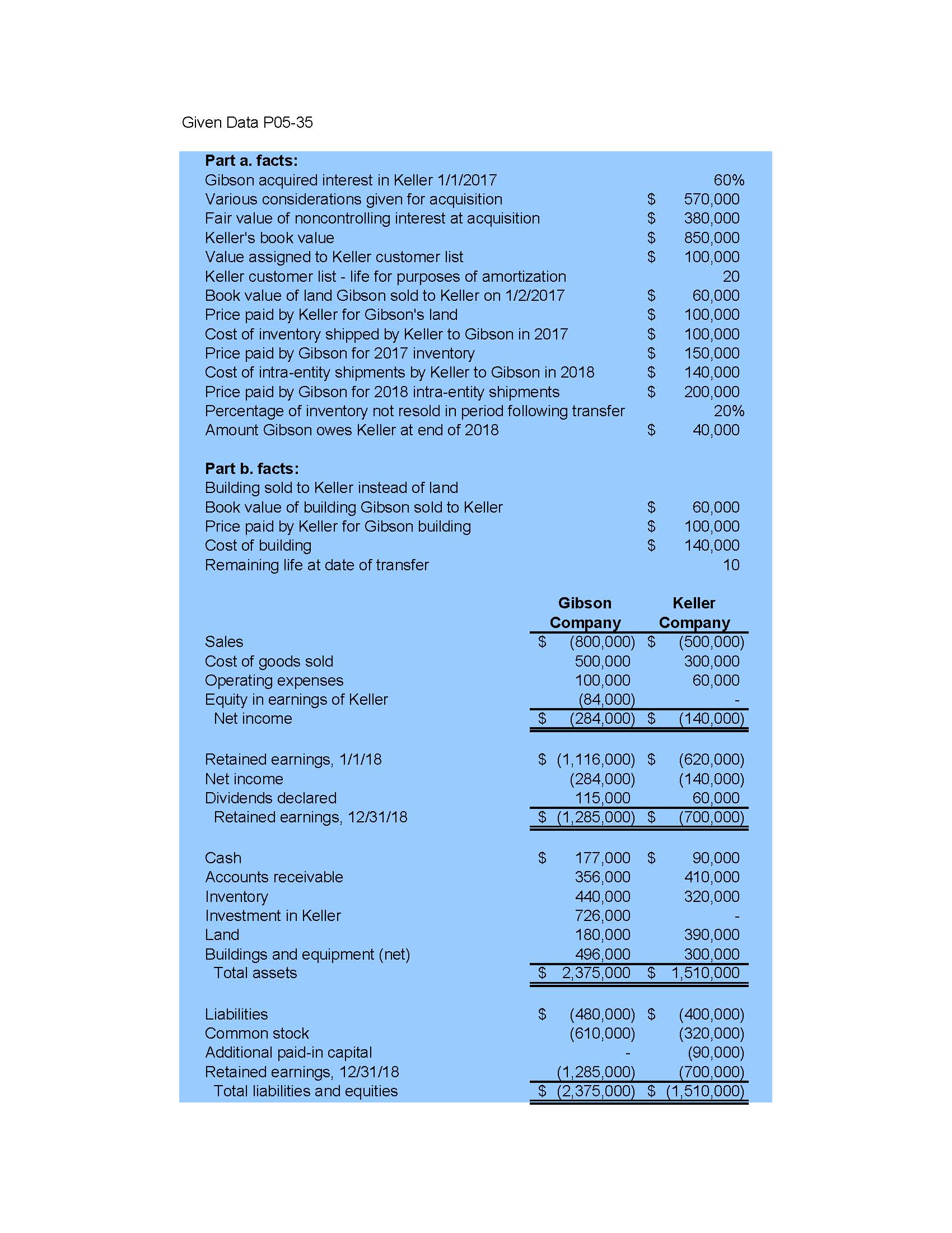

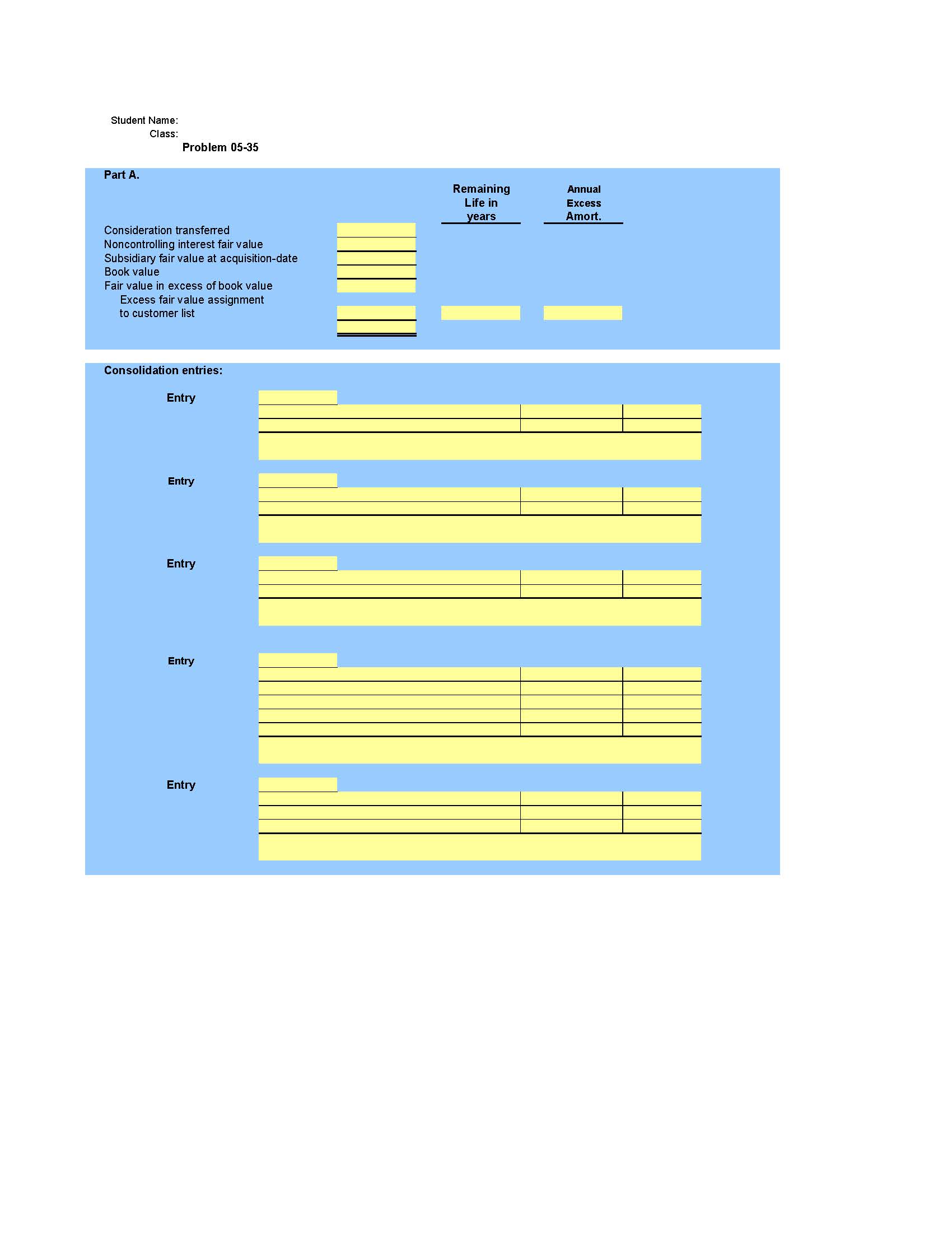

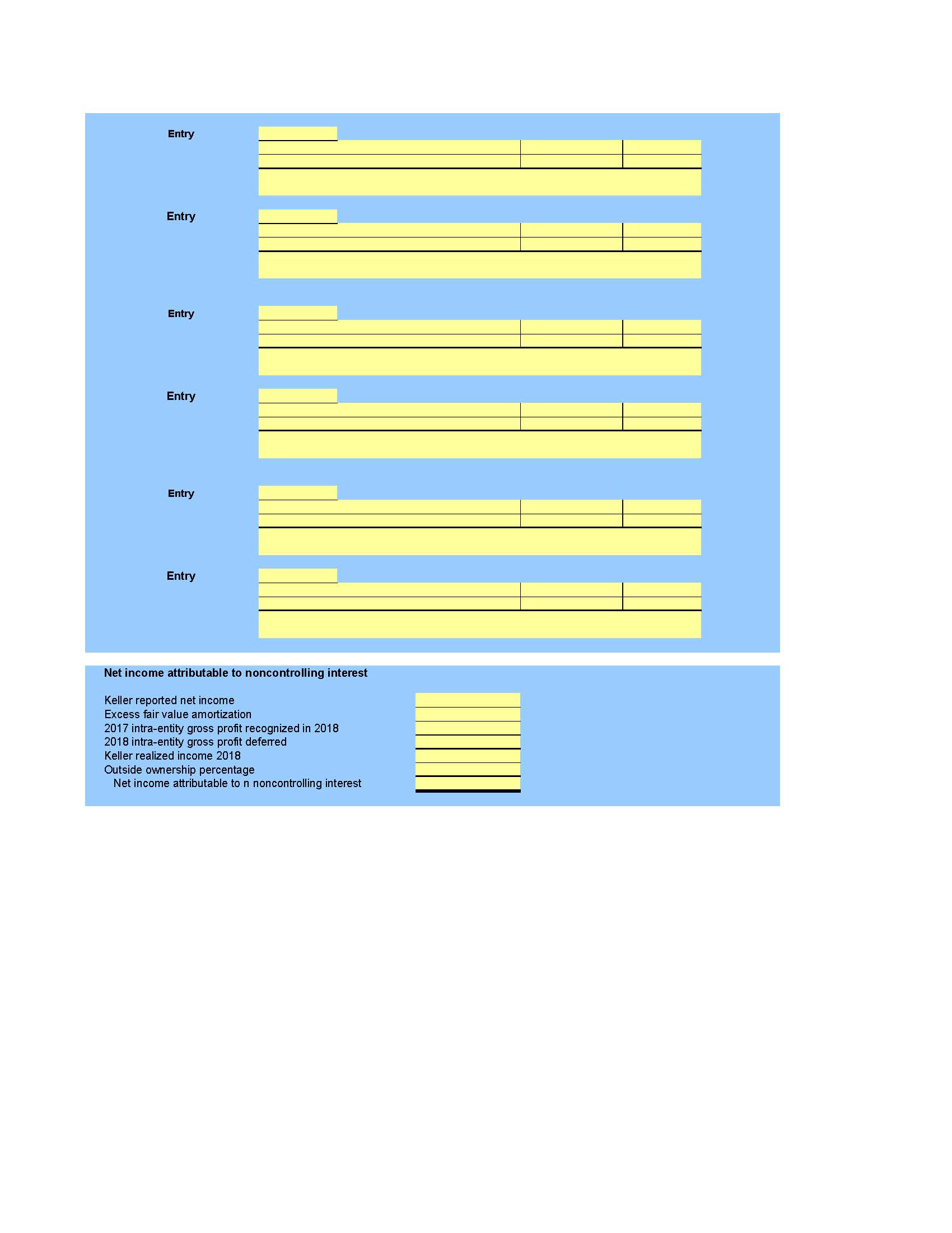

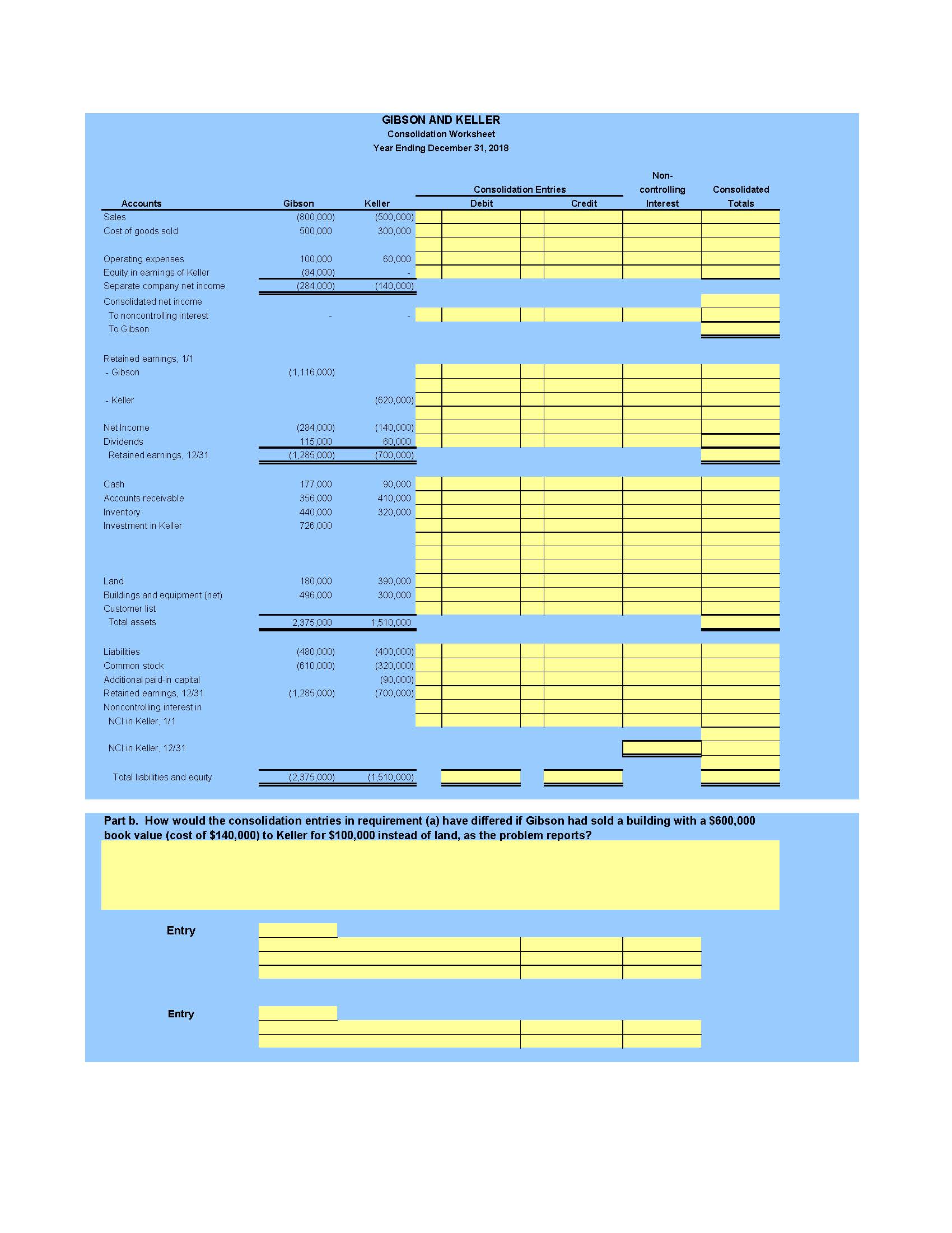

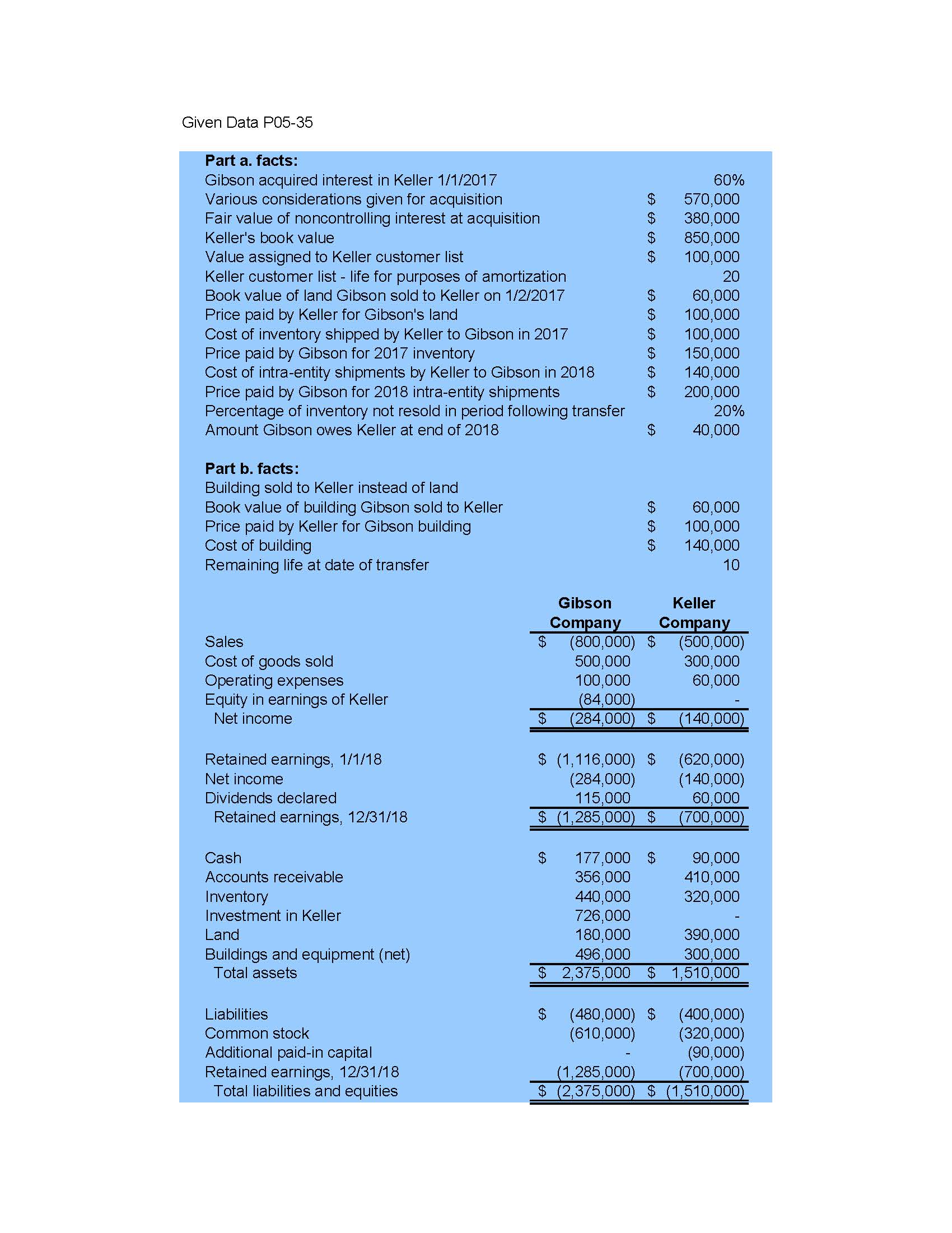

Student Name Class: Problem 05-35 Part A. Remaining Annual Life in Excess years Amort. Consideration transferred Noncontrolling interest fair value Subsidiary fair value at acquisition-date Book value Fair value in excess of book value Excess fair value assignment to customer list Consolidation entries: Entry Entry Entry Entry EntryEntry Entry Entry Entry Entry Entry Net income attributable to noncontrolling interest Keller reported net income Excess fair value amortization 2017 intra-entity gross profit recognized in 2018 2018 intra-entity gross profit deferred Keller realized income 2018 Outside ownership percentage Net income attributable to n noncontrolling interestGIBSON AND KELLER Consolidation Worksheet Year Ending December 31, 2018 Non- Consolidation Entries controlling Accounts Keller Consolidated Gibson Debit Credit Interest Totals Sales (800,000) Cost of goods sold 500,000 (500,000) 00,000 Operating expenses 100,000 60,000 Equity in earnings of Keller (84,000 ) Separate company net income (284,000) (140,000 Consolidated net income To noncontrolling interest To Gibson Retained earnings, 1/1 - Gibson (1,116,000) . Keller (620,000 Net Income 284,000 140,000) Dividends 15,000 60,000 Retained earnings, 12/31 (1,285,000) /00,000) Cash 177,000 90,000 Accounts receivable 356,000 410,000 Inventory 440,000 320,000 Investment in Keller 726,000 Land 180,000 390,00 Buildings and equipment (net) 496,000 300,000 Customer list Total assets 2,375,000 1,510,000 Liabilities (480,000) (400,000 Common stock (610,000) (320,000) Additional paid-in capital (90,000) Retained earnings, 12/31 (1,285,000) (700,000) Joncontrolling interest in NCI in Keller , 1/1 NCI in Keller, 12/31 Total liabilities and equity (2,375,000) (1,510,000) Part b. How would the consolidation entries in requirement (a) have differed if Gibson had sold a building with a $600,000 book value (cost of $140,000) to Keller for $100,000 instead of land, as the problem reports? Entry EntryGiven Data P05-35 Part a. facts: Gibson acquired interest in Keller 1/1/2017 60% Various considerations given for acquisition 570,000 Fair value of noncontrolling interest at acquisition 380,000 Keller's book value 850,000 Value assigned to Keller customer list 100,000 Keller customer list - life for purposes of amortization 20 Book value of land Gibson sold to Keller on 1/2/2017 60,000 Price paid by Keller for Gibson's land 100,000 Cost of inventory shipped by Keller to Gibson in 2017 100,000 Price paid by Gibson for 2017 inventory 150,000 Cost of intra-entity shipments by Keller to Gibson in 2018 140,000 Price paid by Gibson for 2018 intra-entity shipments 200,000 Percentage of inventory not resold in period following transfer 20% Amount Gibson owes Keller at end of 2018 40,000 Part b. facts: Building sold to Keller instead of land Book value of building Gibson sold to Keller 60,000 Price paid by Keller for Gibson building 100,000 Cost of building 140,000 Remaining life at date of transfer 10 Gibson Keller Company Company Sales $ 800,000) $ (500,000) Cost of goods sold 500,000 300,000 Operating expenses 100,000 60,000 Equity in earnings of Keller (84,000 Net income $ 284,000) $ (140,000) Retained earnings, 1/1/18 $ (1, 116,000) $ (620,000) Net income 284,000 (140,000) Dividends declared 115,000 60,000 Retained earnings, 12/31/18 $ (1,285,000) $ (700,000) Cash $ 177,000 $ 90,000 Accounts receivable 356,000 410,000 Inventory 440,000 320,000 Investment in Keller 726,000 Land 180,000 390,000 Buildings and equipment (net) 496,000 300,000 Total assets $ 2,375,000 $ 1,510,000 Liabilities $ (480,000) $ (400,000) Common stock (610,000) 320,000 Additional paid-in capital (90,000) Retained earnings, 12/31/18 (1,285,000) (700,000) Total liabilities and equities $ (2,375,000) $ (1,510,000)