subject: economics hello tutor the answer in the question below is just need to handwrite it because i cannot understand some symbols. please rewrite the

subject: economics

hello tutor the answer in the question below is just need to handwrite it because i cannot understand some symbols.

please rewrite the answers

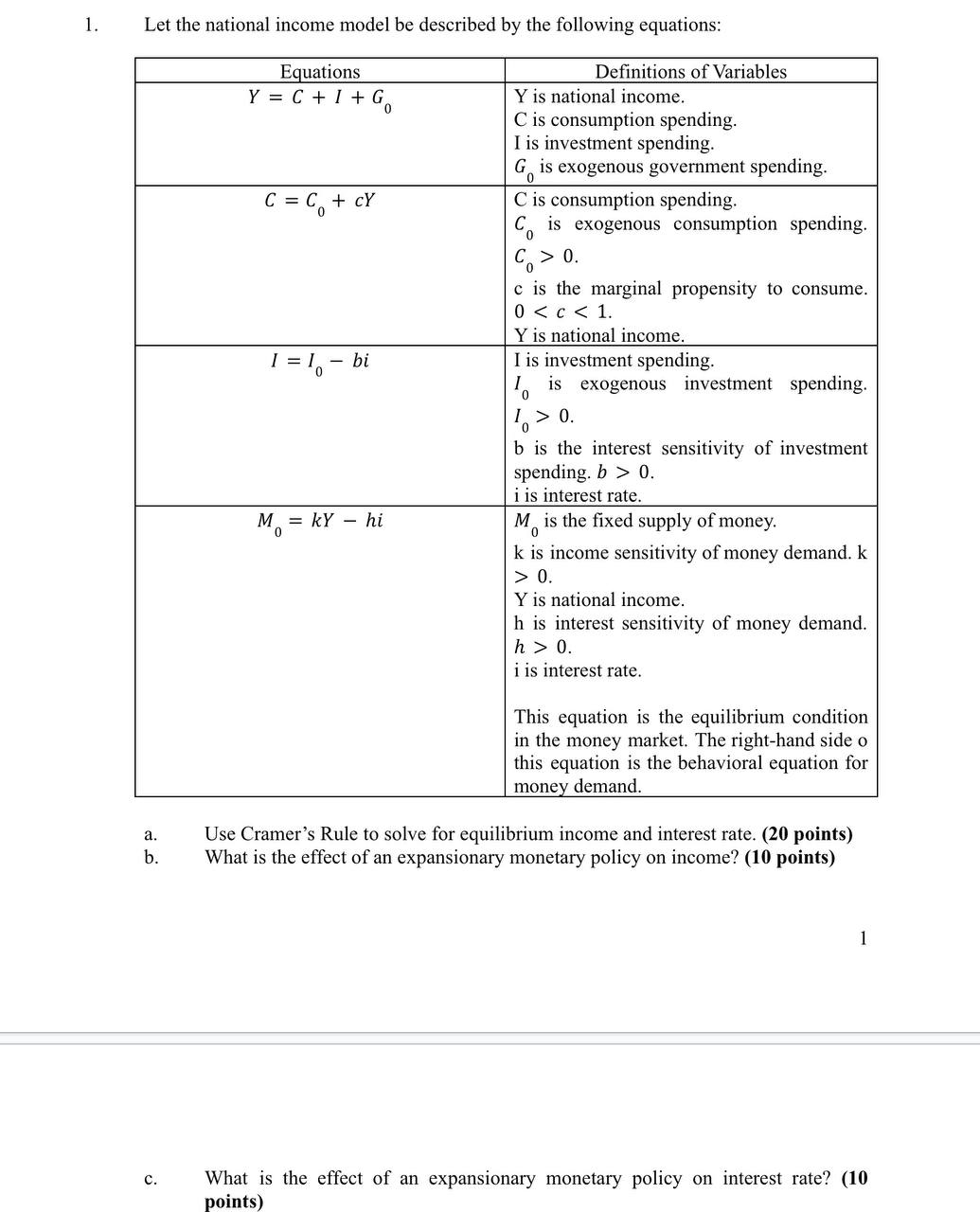

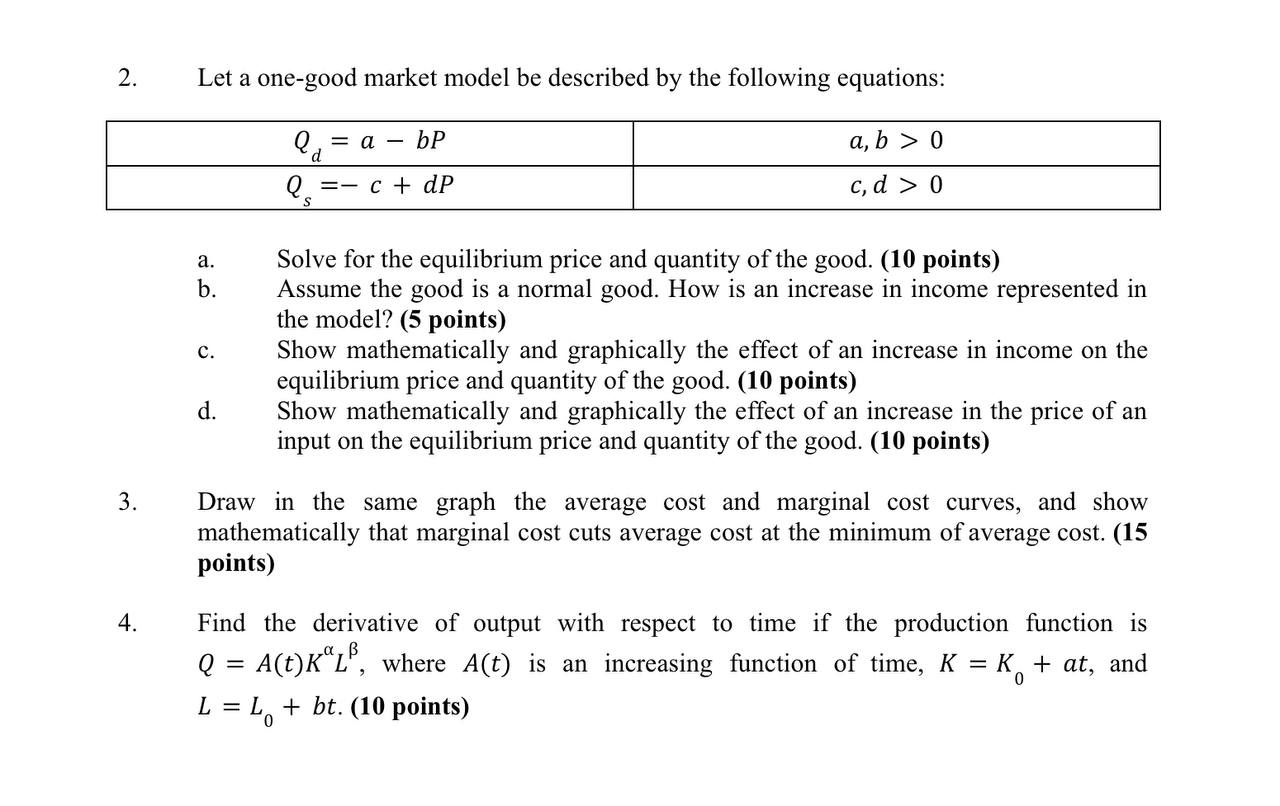

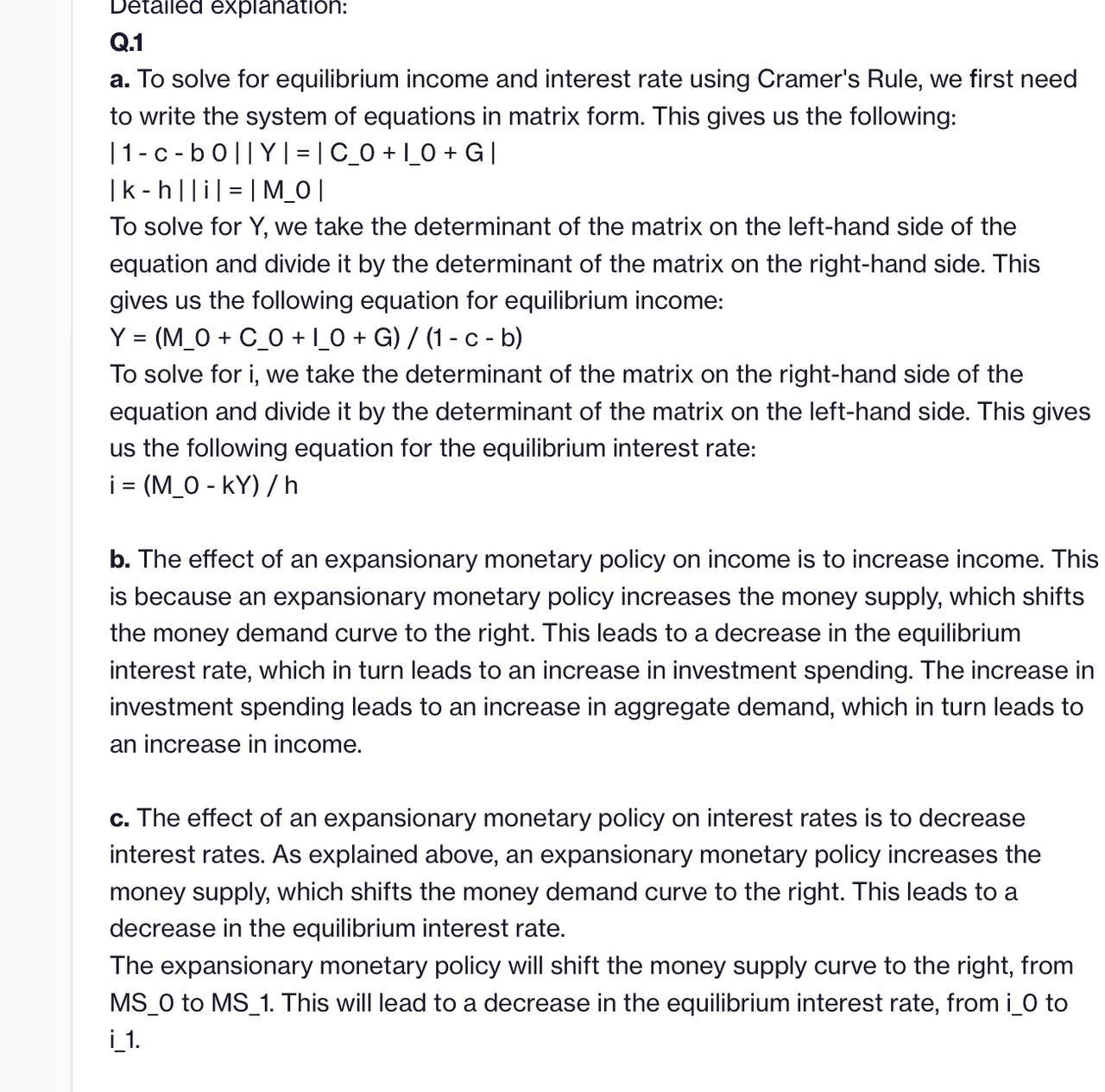

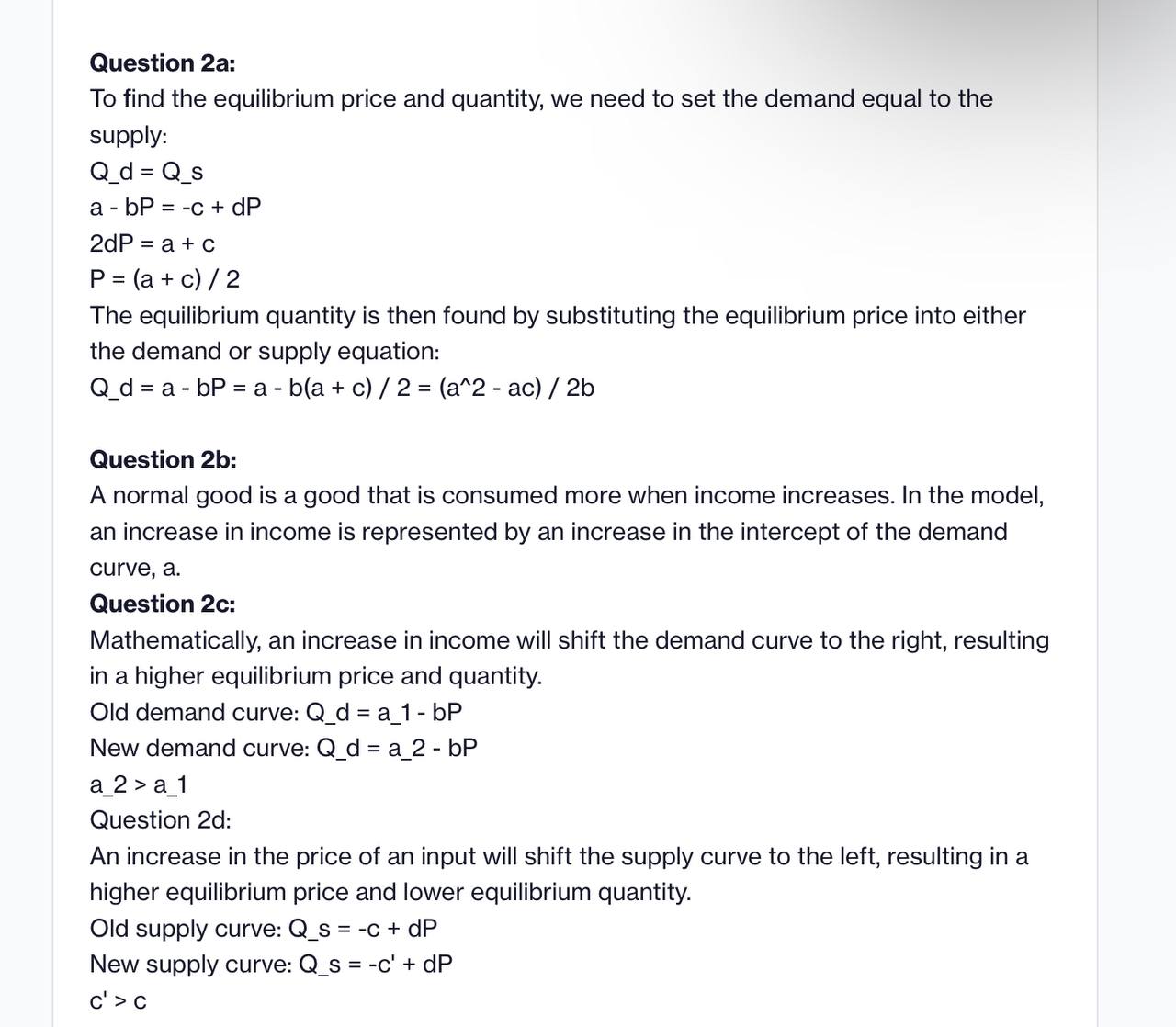

1. Let the national income model be described by the following equations: Denitions of Variables Y is national income. C is consumption spending. I is investment spending. an is exogenous government spending. C is consumption spending. C0 is exogenous consumption spending. CU>D. c is the marginal propensity to consume. 0 U. b is the interest sensitivity of investment spending. is > D. i is interest rate. Mo = id\" hi M is the xed supply ofmoney. k is income sensitivity of money demand. k > {1. Y is national income. h is interest sensitivity of money demand. it > O. i is interest rate. This equation is the equilibrium condition in the money market. The righthand side 0 this equation is the behavioral equation for money demand. a. Use Cramer's Rule to solve for equilibrium income and interest rate. (20 points) in. What is the effect of an expansionary monetary policy on income? (10 points} 1 c. What is the effect of an expansionary monetary policy on interest rate? (10 points) 2. Let a one-good market model be described by the following equations: Q=ic+dP c,d>0 Solve for the equilibrium price and quantity of the good. (10 points) Assume the good is a normal good. How is an increase in income represented in the model? (5 points) 0. Show mathematically and graphically the effect of an increase in income on the equilibrium price and quantity of the good. (10 points) (1. Show mathematically and graphically the effect of an increase in the price of an input on the equilibrium price and quantity of the good. (10 points) 9"?\" Draw in the same graph the average cost and marginal cost curves, and Show mathematically that marginal cost cuts average cost at the minimum of average cost. (15 points) Find the derivative of output with respect to time if the production function is Q = A(t)KaLB, where AG) is an increasing function of time, K = K0 + at, and L = Lo + br. (10 points) UGIalleCl explanation: 0.1 a. To solve for equilibrium income and interest rate using Cramer's Rule, we first need to write the system of equations in matrix form. This gives us the following: |1-c-b0||Y|=|C_0+I_O+G| lk-h||i|=|M_0| To solve for Y, we take the determinant of the matrix on the left-hand side of the equation and divide it by the determinant of the matrix on the right-hand side. This gives us the following equation for equilibrium income: Y=(M_0+C_0+l_0+G)/(1-c-b) To solve for i, we take the determinant of the matrix on the right-hand side of the equation and divide it by the determinant of the matrix on the left-hand side. This gives us the following equation for the equilibrium interest rate: i=(M_O-le/h b. The effect of an expansionary monetary policy on income is to increase income. This is because an expansionary monetary policy increases the money supply, which shifts the money demand curve to the right. This leads to a decrease in the equilibrium interest rate, which in turn leads to an increase in investment spending. The increase in investment spending leads to an increase in aggregate demand, which in turn leads to an increase in income. c. The effect of an expansionary monetary policy on interest rates is to decrease interest rates. As explained above, an expansionary monetary policy increases the money supply, which shifts the money demand curve to the right. This leads to a decrease in the equilibrium interest rate. The expansionary monetary policy will shift the money supply curve to the right, from MS_O to MS_1. This will lead to a decrease in the equilibrium interest rate, from LG to i_1. Question 2a: To find the equilibrium price and quantity, we need to set the demand equal to the supply: Q_d = Q_s a - bP 2 -c + dP 2dP = a + C P = (a + c) / 2 The equilibrium quantity is then found by substituting the equilibrium price into either the demand or supply equation: Q_d=a-bP=a-b(a+c)/2=(a"2-ac)/2b Question 2b: A normal good is a good that is consumed more when income increases. In the model, an increase in income is represented by an increase in the intercept of the demand curve, a. Question 2c: Mathematically, an increase in income will shift the demand curve to the right, resulting in a higher equilibrium price and quantity. Old demand curve: Q_d = a_1 - bP New demand curve: Q_d = a_2 bP a_2 > a_1 Question 2d: An increase in the price of an input will shift the supply curve to the left, resulting in a higher equilibrium price and lower equilibrium quantity. Old supply curve: Q_s = -c + dP New supply curve: Q_s = -c' + dP c' > c Question 2d: An increase in the price of an input will shift the supply curve to the left, resulting in a higher equilibrium price and lower equilibrium quantity. Old supply curve: Q_s = -c + dP New supply curve: Q_s = -c' + dP C' > C Question 3: The average cost curve is defined as the total cost divided by the quantity produced. The marginal cost curve is defined as the change in total cost divided by the change in quantity produced. Average cost = TC / Q Marginal cost = ATC / AQ The relationship between the average cost and marginal cost curves can be shown mathematically as follows: d(AC) / dQ = MC At the minimum of the average cost curve, the derivative of the average cost curve with respect to quantity is equal to zero. This means that the marginal cost curve must cross the average cost curve at its minimum point. Question 4: The derivative of the production function with respect to time is found using the chain rule: dQ / dt = dA / dt * Q + A(t) * d(K^\\alpha L^\\beta) / dt Substituting the given expressions for (K) and (L), we get: dQ / dt = dA / dt * Q + A(t) * ak^(a - 1)at + A(t) * BK^al^(B - 1)bt Finally, we can factor out (A(t)) to get the following expression: do / dt

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance