Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Subject: Financial Modeling - You must show how you do your solutions and all the steps. You also need to show the formulas you use.

Subject: Financial Modeling

- You must show how you do your solutions and all the steps. You also need to show the formulas you use. You are expected to interpret the results obtained

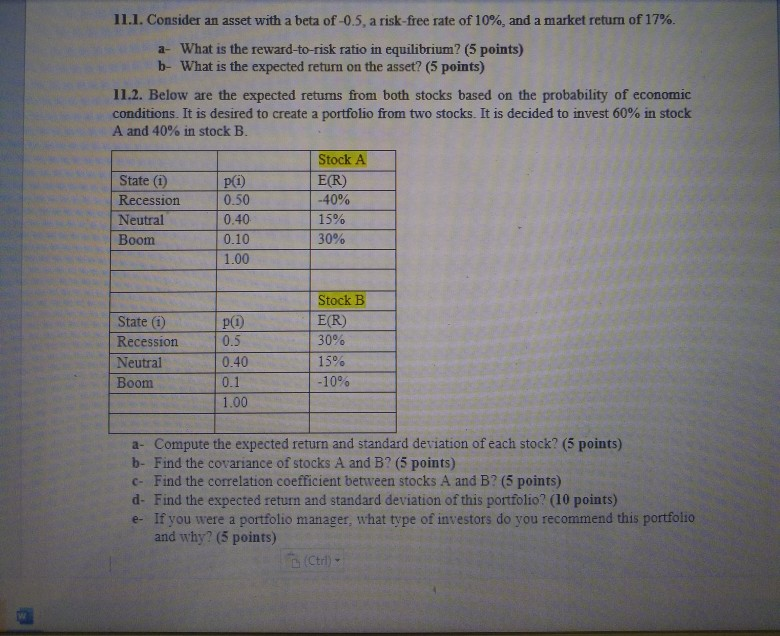

11.1. Consider an asset with a beta of-0.5, a risk-free rate of 10%, and a market return of 17%. a- What is the reward-to-risk ratio in equilibrium? (5 points) b- What is the expected return on the asset? (5 points) 11.2. Below are the expected returns from both stocks based on the probability of economic conditions. It is desired to create a portfolio from two stocks. It is decided to invest 60% in stock A and 40% in stock B. State (1) Recession Neutral Boom p(i) 0.50 0.40 0.10 1.00 Stock A E(R) -40% 15% 30% ) State (1) Recession Neutral Boom 0.5 0.40 0.1 1.00 Stock B E(R) 30% 15% -10% a- Compute the expected return and standard deviation of each stock? (5 points) b- Find the covariance of stocks A and B? (5 points) C- Find the correlation coefficient between stocks A and B? (5 points) d. Find the expected return and standard deviation of this portfolio? (10 points) - If you were a portfolio manager, what type of investors do you recommend this portfolio and why? (5 points) (Ctrl)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction Volume 2

Authors: Piotr Staszkiewicz, Lucia Staszkiewicz

1st Edition

0128027975, 978-0128027974