Answered step by step

Verified Expert Solution

Question

1 Approved Answer

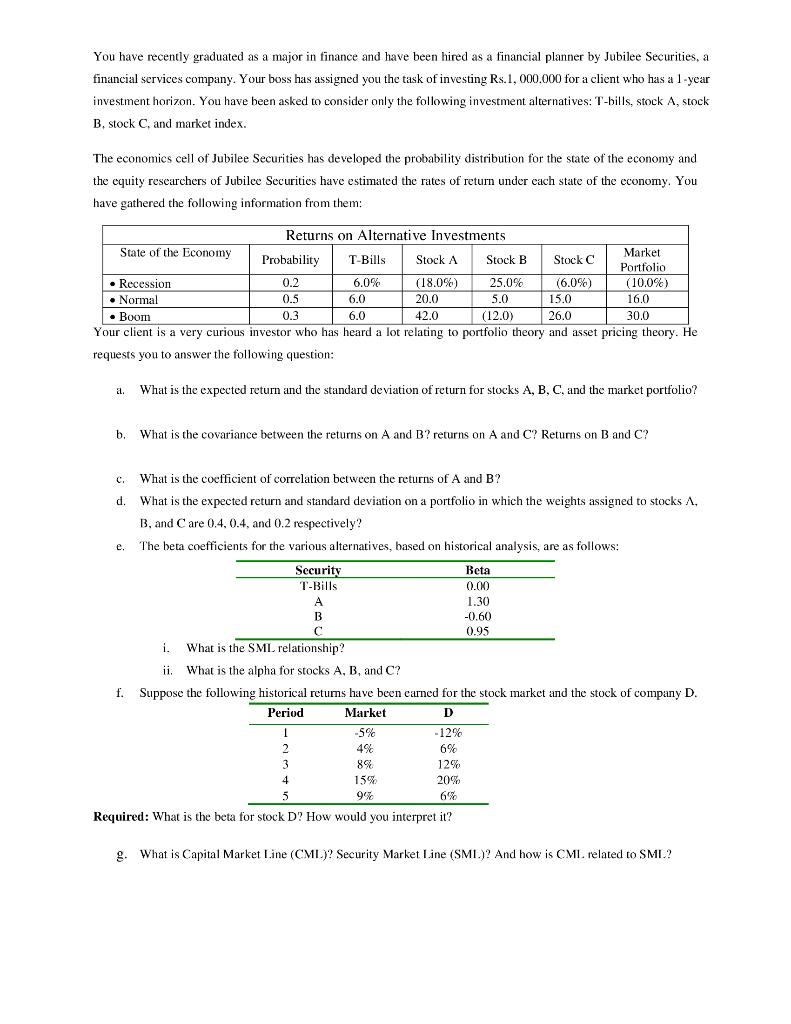

Subject: Investment and Portfolio Management You have recently graduated as a major in finance and have been hired as a financial planner by Jubilee Securities,

Subject: Investment and Portfolio Management

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Create Wealth How You Can Ditch The 9 5 Job With Multifamily Investing

Authors: Pam Scamardo

1st Edition

979-8986637709