Answered step by step

Verified Expert Solution

Question

1 Approved Answer

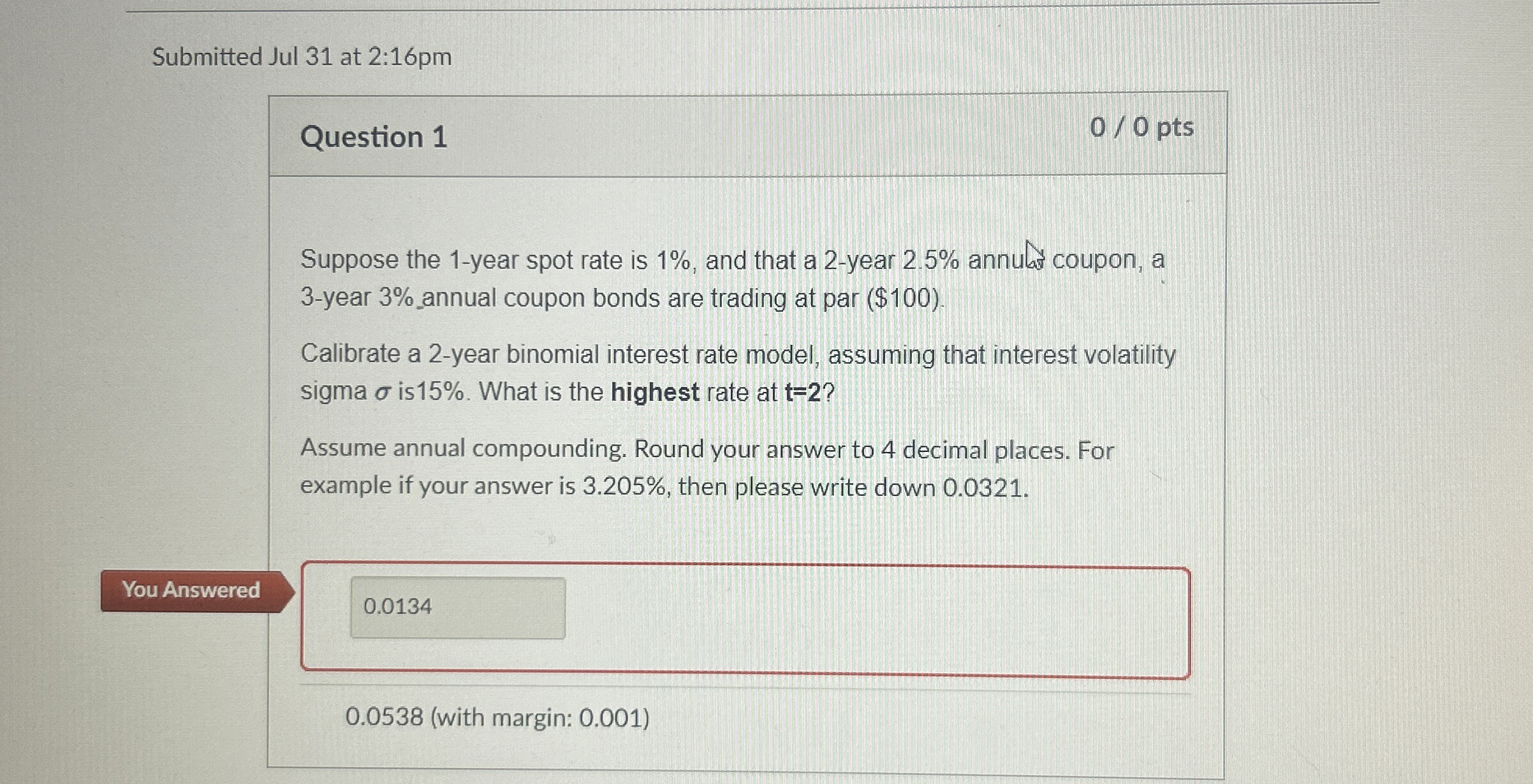

Submitted Jul 3 1 at 2 : 1 6 pm Question 1 0 0 pts Suppose the 1 - year spot rate is 1 %

Submitted Jul at :pm

Question

pts

Suppose the year spot rate is and that a year annulas coupon, a year annual coupon bonds are trading at par $

Calibrate a year binomial interest rate model, assuming that interest volatility sigma is What is the highest rate at

Assume annual compounding. Round your answer to decimal places. For example if your answer is then please write down

with margin:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Credit Spreads Beginners Guide To Low Risk Secure Easy To Manage Consistent Profits For Long Term Wealth Creation

Authors: Casey Boon

1st Edition

1974677419, 978-1974677412