Answered step by step

Verified Expert Solution

Question

1 Approved Answer

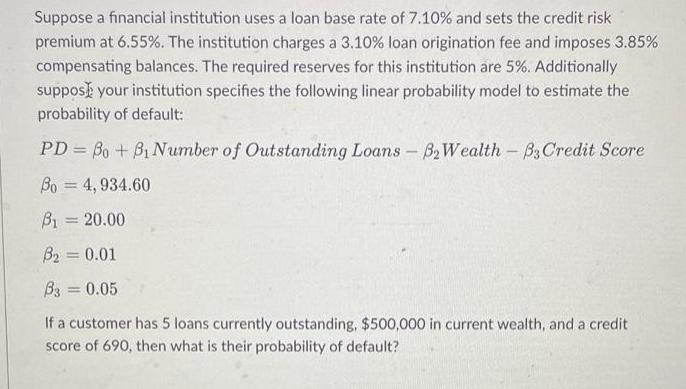

Suppose a financial institution uses a loan base rate of 7.10% and sets the credit risk premium at 6.55%. The institution charges a 3.10%

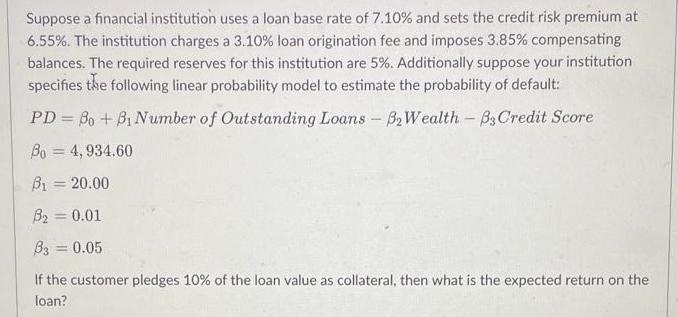

Suppose a financial institution uses a loan base rate of 7.10% and sets the credit risk premium at 6.55%. The institution charges a 3.10% loan origination fee and imposes 3.85% compensating balances. The required reserves for this institution are 5%. Additionally suppose your institution specifies the following linear probability model to estimate the probability of default: PD Bo + B1 Number of Outstanding Loans - B Wealth - B3 Credit Score Bo = 4,934.60 B20.00 B = 0.01 B3 = 0.05 If a customer has 5 loans currently outstanding, $500,000 in current wealth, and a credit score of 690, then what is their probability of default? Suppose a financial institution uses a loan base rate of 7.10% and sets the credit risk premium at 6.55%. The institution charges a 3.10% loan origination fee and imposes 3.85% compensating balances. The required reserves for this institution are 5%. Additionally suppose your institution specifies the following linear probability model to estimate the probability of default: PD = Bo + B1 Number of Outstanding Loans - B Wealth - B3 Credit Score Bo = 4,934.60 B = 20.00 B = 0.01 B3 = 0.05 If the customer pledges 10% of the loan value as collateral, then what is the expected return on the loan?

Step by Step Solution

★★★★★

3.34 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the probability of default PD we can use the linear probability model specified PD Bo B ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management and Financial Institutions

Authors: Hull John

4th edition

1118955943, 978-1118955949