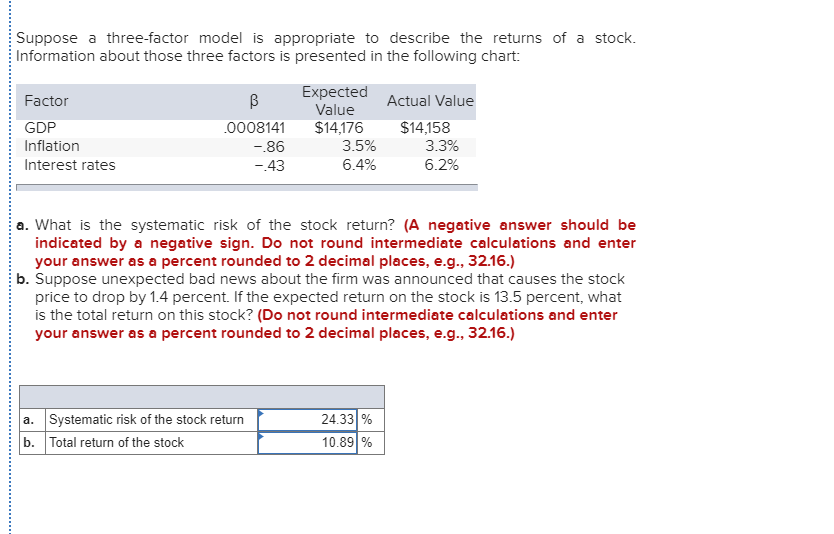

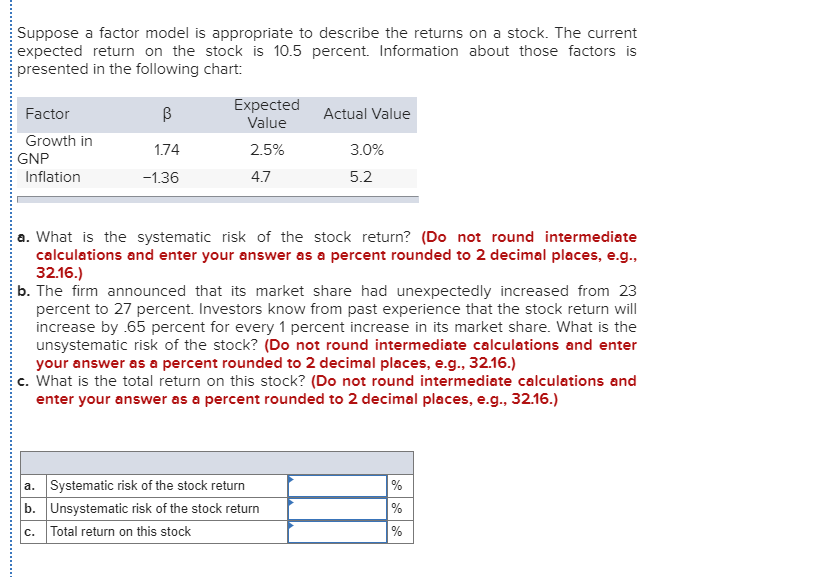

Suppose a three-factor model is appropriate to describe the returns of a stock. Information about those three factors is presented in the following chart: B Expected Actual Value Factor GDP Inflation Interest rates .0008141 Value $14,176 3.5% 6.4% -.86 $14,158 3.3% 6.2% - 43 a. What is the systematic risk of the stock return? (A negative answer should be indicated by a negative sign. Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. Suppose unexpected bad news about the firm was announced that causes the stock price to drop by 1.4 percent. If the expected return on the stock is 13.5 percent, what is the total return on this stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Systematic risk of the stock return Total return of the stock 24.33 % 10.89% b. Suppose a factor model is appropriate to describe the returns on a stock. The current expected return on the stock is 10.5 percent. Information about those factors is presented in the following chart: Expected Factor Actual Value Value 2.5% Growth in GNP Inflation 1.74 -1.36 3.0% 5.2 4.7 a. What is the systematic risk of the stock return? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. The firm announced that its market share had unexpectedly increased from 23 percent to 27 percent. Investors know from past experience that the stock return will increase by .65 percent for every 1 percent increase in its market share. What is the unsystematic risk of the stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) c. What is the total return on this stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) a. Systematic risk of the stock return b. Unsystematic risk of the stock return c. Total return on this stock Suppose a three-factor model is appropriate to describe the returns of a stock. Information about those three factors is presented in the following chart: B Expected Actual Value Factor GDP Inflation Interest rates .0008141 Value $14,176 3.5% 6.4% -.86 $14,158 3.3% 6.2% - 43 a. What is the systematic risk of the stock return? (A negative answer should be indicated by a negative sign. Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. Suppose unexpected bad news about the firm was announced that causes the stock price to drop by 1.4 percent. If the expected return on the stock is 13.5 percent, what is the total return on this stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Systematic risk of the stock return Total return of the stock 24.33 % 10.89% b. Suppose a factor model is appropriate to describe the returns on a stock. The current expected return on the stock is 10.5 percent. Information about those factors is presented in the following chart: Expected Factor Actual Value Value 2.5% Growth in GNP Inflation 1.74 -1.36 3.0% 5.2 4.7 a. What is the systematic risk of the stock return? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. The firm announced that its market share had unexpectedly increased from 23 percent to 27 percent. Investors know from past experience that the stock return will increase by .65 percent for every 1 percent increase in its market share. What is the unsystematic risk of the stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) c. What is the total return on this stock? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) a. Systematic risk of the stock return b. Unsystematic risk of the stock return c. Total return on this stock