Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Suppose ABC Ltd. is a South African company that imports Omega Swiss Watches from Switzerland. On 1 November 2022, ABC Ltd. placed an order

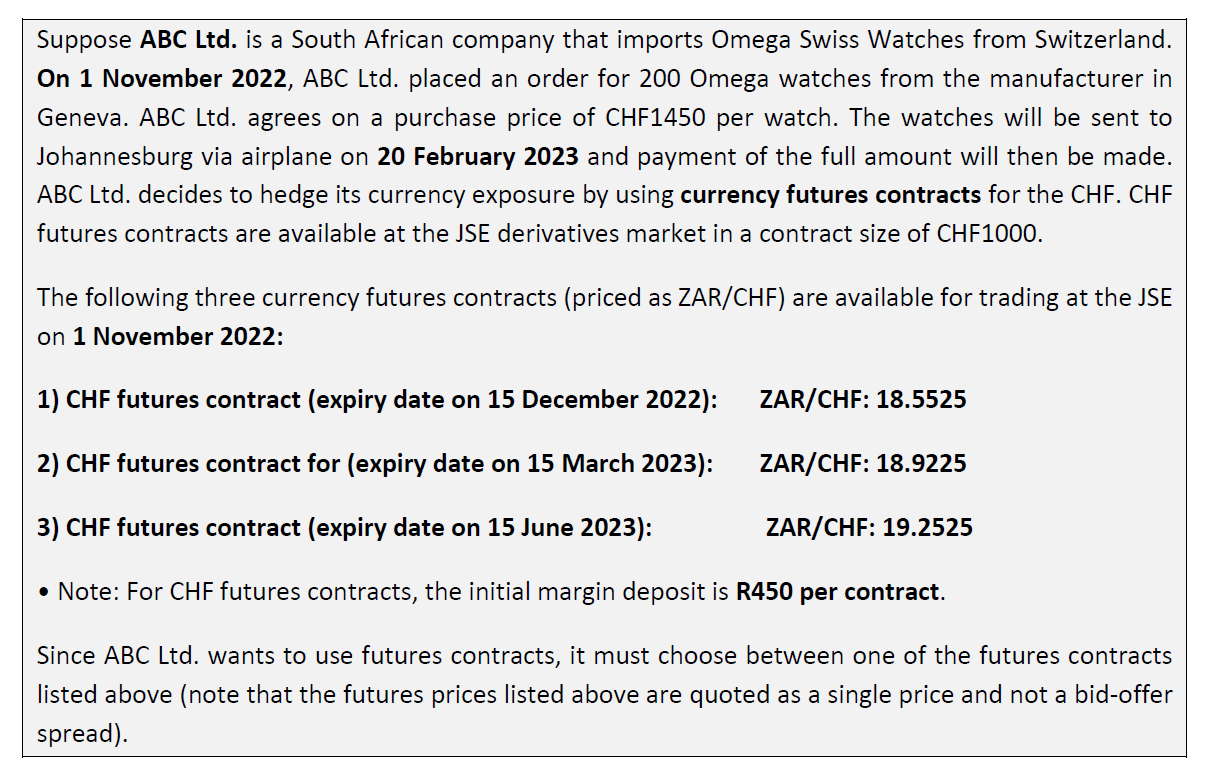

Suppose ABC Ltd. is a South African company that imports Omega Swiss Watches from Switzerland. On 1 November 2022, ABC Ltd. placed an order for 200 Omega watches from the manufacturer in Geneva. ABC Ltd. agrees on a purchase price of CHF1450 per watch. The watches will be sent to Johannesburg via airplane on 20 February 2023 and payment of the full amount will then be made. ABC Ltd. decides to hedge its currency exposure by using currency futures contracts for the CHF. CHF futures contracts are available at the JSE derivatives market in a contract size of CHF1000. The following three currency futures contracts (priced as ZAR/CHF) are available for trading at the JSE on 1 November 2022: 1) CHF futures contract (expiry date on 15 December 2022): 2) CHF futures contract for (expiry date on 15 March 2023): ZAR/CHF: 18.9225 3) CHF futures contract (expiry date on 15 June 2023): ZAR/CHF: 19.2525 Note: For CHF futures contracts, the initial margin deposit is R450 per contract. Since ABC Ltd. wants to use futures contracts, it must choose between one of the futures contracts listed above (note that the futures prices listed above are quoted as a single price and not a bid-offer spread). ZAR/CHF: 18.5525 2.1 2.2 2.3 2.4 2.5 2.6 2.7 ABC Ltd. must decide if the hedged position for the CHF will be long or short. Explain which position (long or short) must be taken and why. (2) Which futures contract will be best to use, and why? (2) Given your answer above, explain what purchase amount (in ZAR) would ABC Ltd. be able to budget for in terms of this import transaction? (3) How many futures contracts should be bought/sold by ABC Ltd? Explain. (3) Based on your answer above explain what the initial margin deposit (in ZAR) will be that ABC Ltd. must make with its derivatives market broker. (3) UFS BUSINESS SCHOOL BE WORTH MORE Illustrate (i.e., draw a futures payoff graph) to explain the futures position of ABC Ltd. (3) Suppose it is now 20 February 2023 and the watches arrive in Johannesburg. Suppose the March 2023 and June 2023 futures contracts for the CHF trade at the following exchange rates:

Step by Step Solution

★★★★★

3.39 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

21 ABC Ltd needs to take a short position in the CHF futures contract as it has an obligation to pay ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Core Principles and Applications

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

5th edition

1259289907, 978-1259289903