Answered step by step

Verified Expert Solution

Question

1 Approved Answer

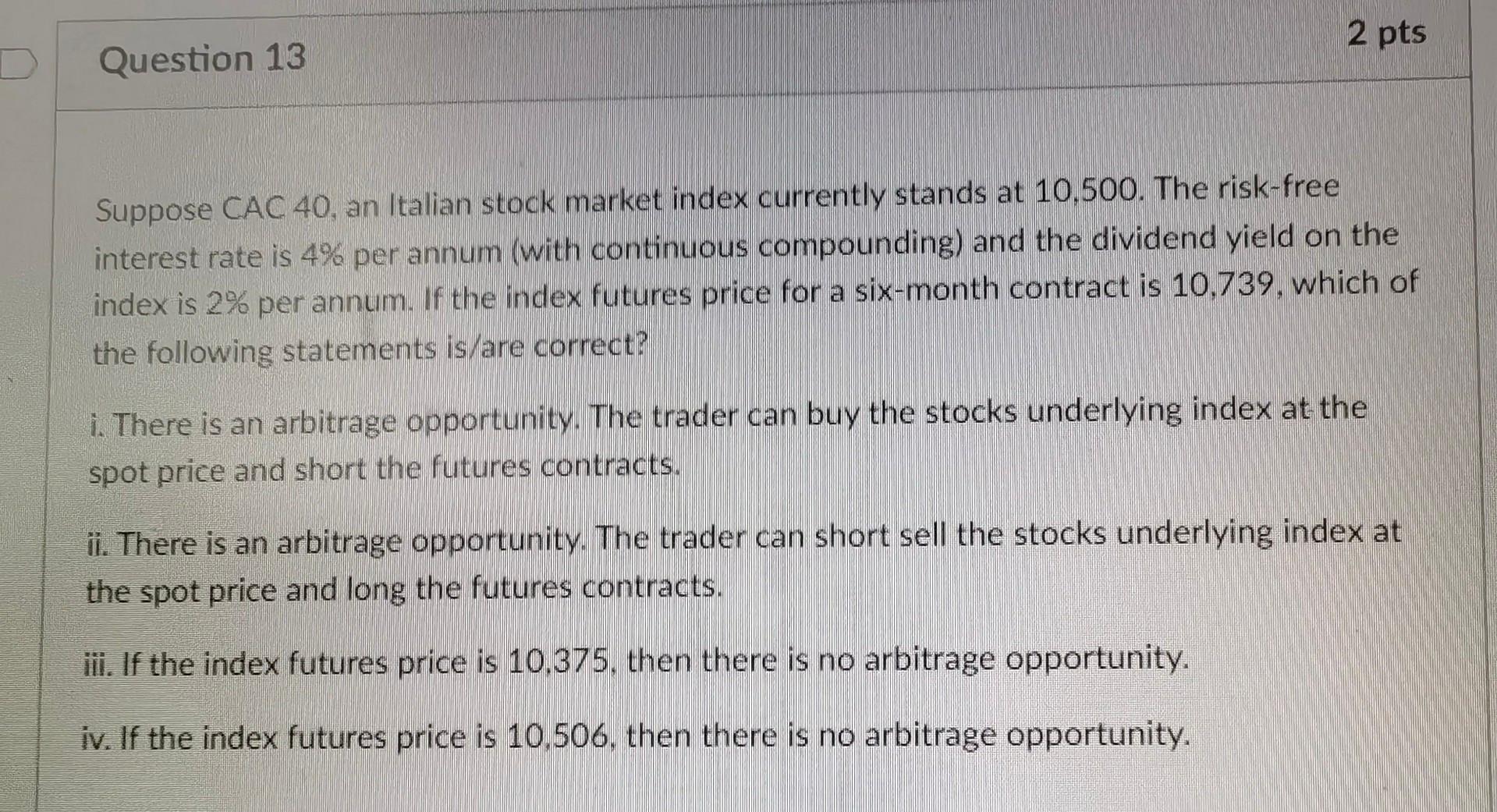

Suppose CAC 40, an Italian stock market index currently stands at 10,500. The risk-free interest rate is 4% per annum (with continuous compounding) and the

Suppose CAC 40, an Italian stock market index currently stands at 10,500. The risk-free interest rate is 4% per annum (with continuous compounding) and the dividend yield on the index is 2% per annum. If the index futures price for a six-month contract is 10,739 , which of the following statements is/are correct? i. There is an arbitrage opportunity. The trader can buy the stocks underlying index at the spot price and short the futures contracts. ii. There is an arbitrage opportunity. The trader can short sell the stocks underlying index at the spot price and long the futures contracts. iii. If the index futures price is 10,375 , then there is no arbitrage opportunity. iv. If the index futures price is 10,506 , then there is no arbitrage opportunity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Theory Of Constraints Handbook

Authors: James Cox, John Schleier

1st Edition

0071665544, 978-0071665544