Answered step by step

Verified Expert Solution

Question

1 Approved Answer

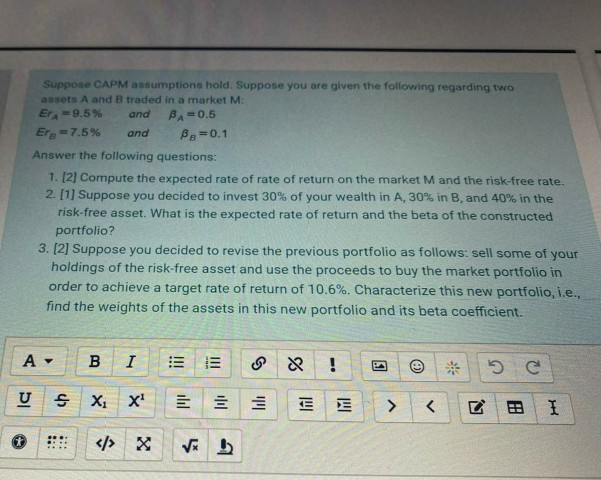

Suppose CAPM assumptions hold. Suppose you are given the following regarding two assets A and B traded in a market M: Eri=9.5% and BA=0.5 Ero

Suppose CAPM assumptions hold. Suppose you are given the following regarding two assets A and B traded in a market M: Eri=9.5% and BA=0.5 Ero 7.5% and Ba=0.1 Answer the following questions: 1. [2) Compute the expected rate of rate of return on the market M and the risk-free rate. 2. [1] Suppose you decided to invest 30% of your wealth in A, 30% in B, and 40% in the risk-free asset. What is the expected rate of return and the beta of the constructed portfolio 3. [2] Suppose you decided to revise the previous portfolio as follows: sell some of your holdings of the risk-free asset and use the proceeds to buy the market portfolio in order to achieve a target rate of return of 10.6%. Characterize this new portfolio, i.e., find the weights of the assets in this new portfolio and its beta coefficient. . B I !!! & ! C ! Ic S X X lili E A IM

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Millionaire Next Door The Surprising Secrets Of Americas Wealthy

Authors: Thomas J. Stanley, William D. Danko

1st Edition

1589795474, 978-1589795471