Answered step by step

Verified Expert Solution

Question

1 Approved Answer

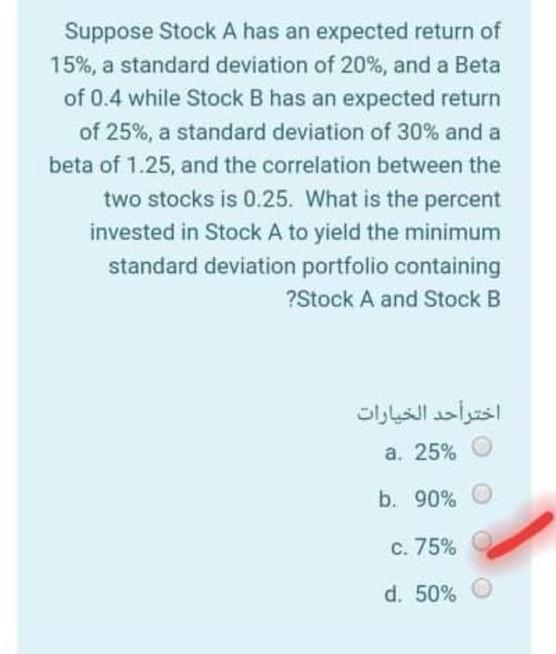

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the percent invested in Stock A to yield the minimum standard deviation portfolio containing ?Stock A and Stock B a. 25% b. 90% c. 75% d. 50%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Quick Master Guide 2023 For Financial Business Growth A Comprehensive Beginners To Expert Guide To Financial And Managerial Accounting And Finance Professionals With Helpful Tips

Authors: Glorified Kathryn

1st Edition

979-8387518461