Answered step by step

Verified Expert Solution

Question

1 Approved Answer

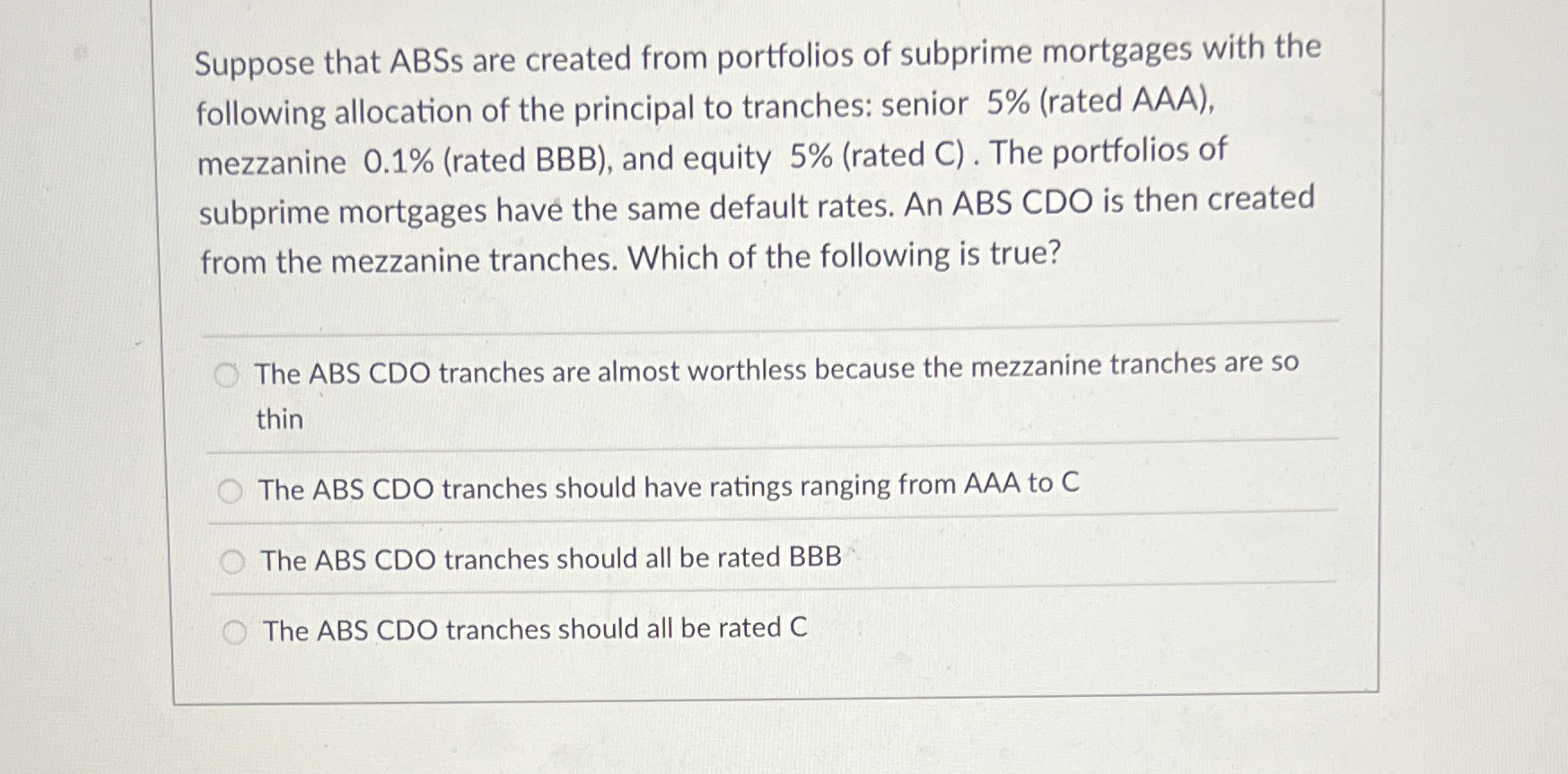

Suppose that ? A B S s are created from portfolios of subprime mortgages with the following allocation of the principal to tranches: senior 5

Suppose that s are created from portfolios of subprime mortgages with the

following allocation of the principal to tranches: senior rated AAA

mezzanine rated BBB and equity rated C The portfolios of

subprime mortgages have the same default rates. An ABS CDO is then created

from the mezzanine tranches. Which of the following is true?

The ABS CDO tranches are almost worthless because the mezzanine tranches are so

thin

The ABS CDO tranches should have ratings ranging from AAA to

The ABS CDO tranches should all be rated BBB

The ABS CDO tranches should all be rated

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Complete Guide To Bitcoin Understand Everything From Getting Started With Bitcoin Sending And Receiving Bitcoin To Mining Bitcoin

Authors: Mr Mark Gates

1st Edition

1974565491, 978-1974565498