Answered step by step

Verified Expert Solution

Question

1 Approved Answer

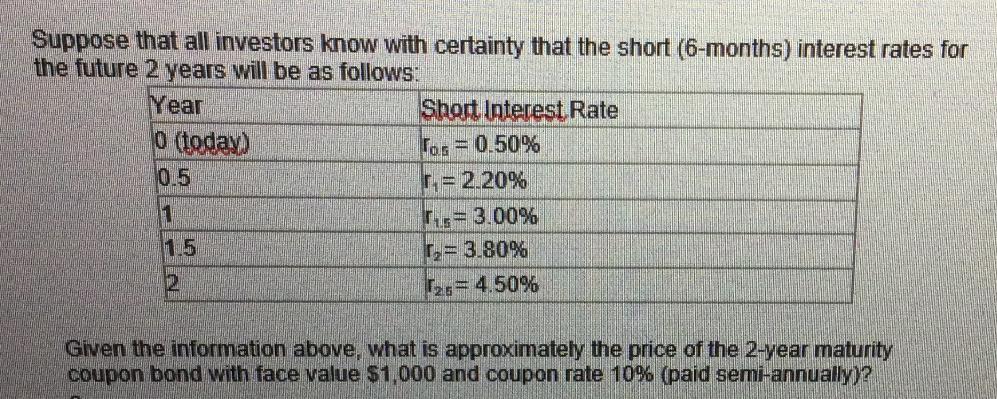

Suppose that all investors know with certainty that the short (6-months) interest rates for the future 2 years will be as follows: Year 0

Suppose that all investors know with certainty that the short (6-months) interest rates for the future 2 years will be as follows: Year 0 (today) 0.5 1 1.5 Short Interest Rate Tos = 0.50% =2.20% = 3.00% r= 3.80% 25= 4.50% Given the information above, what is approximately the price of the 2-year maturity coupon bond with face value $1,000 and coupon rate 10% (paid semi-annually)?

Step by Step Solution

★★★★★

3.31 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the price of the 2year maturity coupon bond we need to discount the future cash flows c...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics An Intuitive Approach with Calculus

Authors: Thomas Nechyba

1st edition

538453257, 978-0538453257