Answered step by step

Verified Expert Solution

Question

1 Approved Answer

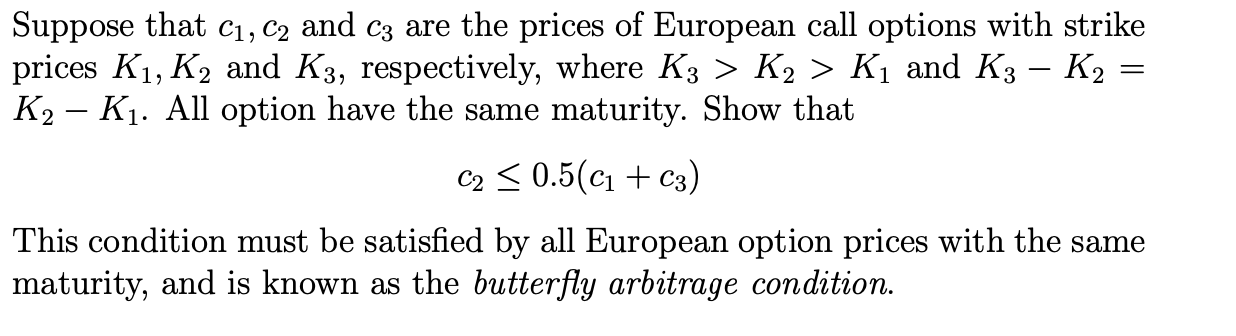

Suppose that c1,c2 and c3 are the prices of European call options with strike prices K1,K2 and K3, respectively, where K3>K2>K1 and K3K2= K2K1. All

Suppose that c1,c2 and c3 are the prices of European call options with strike prices K1,K2 and K3, respectively, where K3>K2>K1 and K3K2= K2K1. All option have the same maturity. Show that c20.5(c1+c3) This condition must be satisfied by all European option prices with the same maturity, and is known as the butterfly arbitrage condition

Suppose that c1,c2 and c3 are the prices of European call options with strike prices K1,K2 and K3, respectively, where K3>K2>K1 and K3K2= K2K1. All option have the same maturity. Show that c20.5(c1+c3) This condition must be satisfied by all European option prices with the same maturity, and is known as the butterfly arbitrage condition Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trade Union Finance

Authors: Marick F. Masters, Raymond Gibney

1st Edition

1032371382, 978-1032371382