Answered step by step

Verified Expert Solution

Question

1 Approved Answer

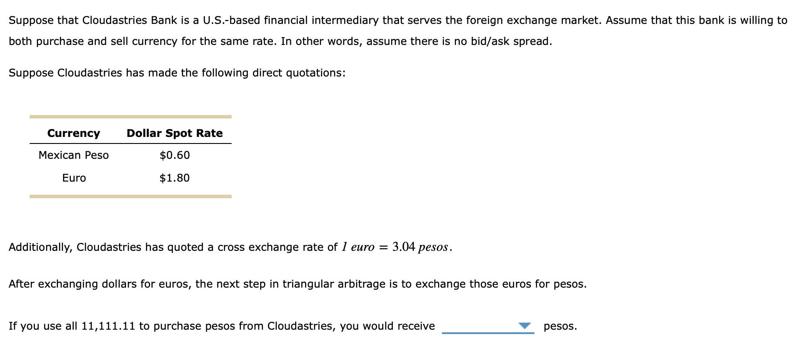

Suppose that Cloudastries Bank is a U.S.-based financial intermediary that serves the foreign exchange market. Assume that this bank is willing to both purchase

Suppose that Cloudastries Bank is a U.S.-based financial intermediary that serves the foreign exchange market. Assume that this bank is willing to both purchase and sell currency for the same rate. In other words, assume there is no bid/ask spread. Suppose Cloudastries has made the following direct quotations: Currency Dollar Spot Rate Mexican Peso $0.60 $1.80 Euro Additionally, Cloudastries has quoted a cross exchange rate of 1 euro = 3.04 pesos. After exchanging dollars for euros, the next step in triangular arbitrage is to exchange those euros for pesos. If you use all 11,111.11 to purchase pesos from Cloudastries, you would receive pesos.

Step by Step Solution

★★★★★

3.56 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

In triangular arbitrage you start with a base currency in this cas...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Spreadsheet Modeling And Decision Analysis A Practical Introduction To Management Science

Authors: Cliff T. Ragsdale

5th Edition

324656645, 324656637, 9780324656640, 978-0324656633