Answered step by step

Verified Expert Solution

Question

1 Approved Answer

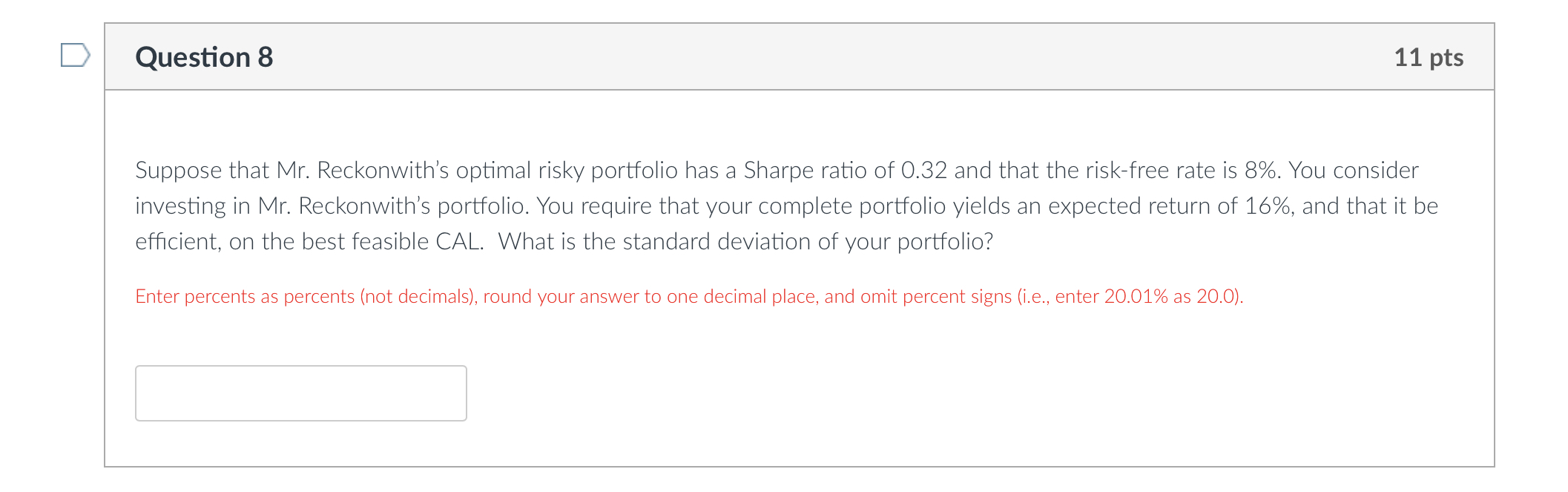

Suppose that Mr. Reckonwith's optimal risky portfolio has a Sharpe ratio of 0.32 and that the risk-free rate is 8%. You consider investing in Mr.

Suppose that Mr. Reckonwith's optimal risky portfolio has a Sharpe ratio of 0.32 and that the risk-free rate is 8%. You consider investing in Mr. Reckonwith's portfolio. You require that your complete portfolio yields an expected return of 16%, and that it be efficient, on the best feasible CAL. What is the standard deviation of your portfolio? Enter percents as percents (not decimals), round your answer to one decimal place, and omit percent signs (i.e., enter 20.01\% as 20.0)

Suppose that Mr. Reckonwith's optimal risky portfolio has a Sharpe ratio of 0.32 and that the risk-free rate is 8%. You consider investing in Mr. Reckonwith's portfolio. You require that your complete portfolio yields an expected return of 16%, and that it be efficient, on the best feasible CAL. What is the standard deviation of your portfolio? Enter percents as percents (not decimals), round your answer to one decimal place, and omit percent signs (i.e., enter 20.01\% as 20.0) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Recent Advances In Commodity And Financial Modeling

Authors: Giorgio Consigli, Silvana Stefani, Giovanni Zambruno

1st Edition

3319613189, 978-3319613185