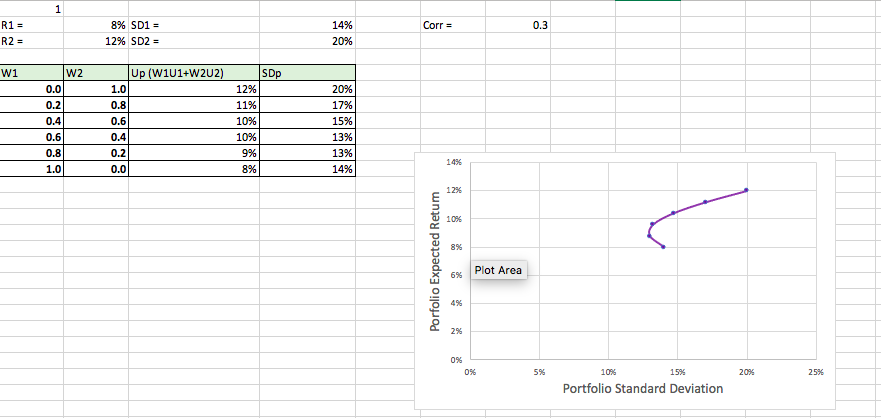

Question

Suppose that one investment has a mean return of 8% and a standard deviation of return of 14%. Another investment has a mean return of

Suppose that one investment has a mean return of 8% and a standard deviation of return of 14%. Another investment has a mean return of 12% and a standard deviation of return of 20%. The correlation between the returns is 0.3. Illustrate in a graph the risk-return trade-off. Please be sure to label the efficient frontier, as well.

This is what I have so far. I need help finding the efficient frontier with an explanation on how to do it. Thank you.

1 14% Corr 0.3 R1 = R2 = 8% SD1 = 12% SD2 = 20% W1 SDp W2 0.01 0.2 0.4 0.6 Up (W1U1+W202) 1.0 0.8 0.6 0.4 0.2 0.0 12% 11% 10% 10% 9% 8% 20% 17% 15% 13% 13% 0.8 1.0 14% 14% 129 10% 8% Porfolio Expected Retum Plot Area 6% 2% 0% 0% 5% 20% 25% 10% 15% Portfolio Standard DeviationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Non Financial Managers

Authors: Gene Siciliano

1st Edition

0071413774, 978-0071413770