Answered step by step

Verified Expert Solution

Question

1 Approved Answer

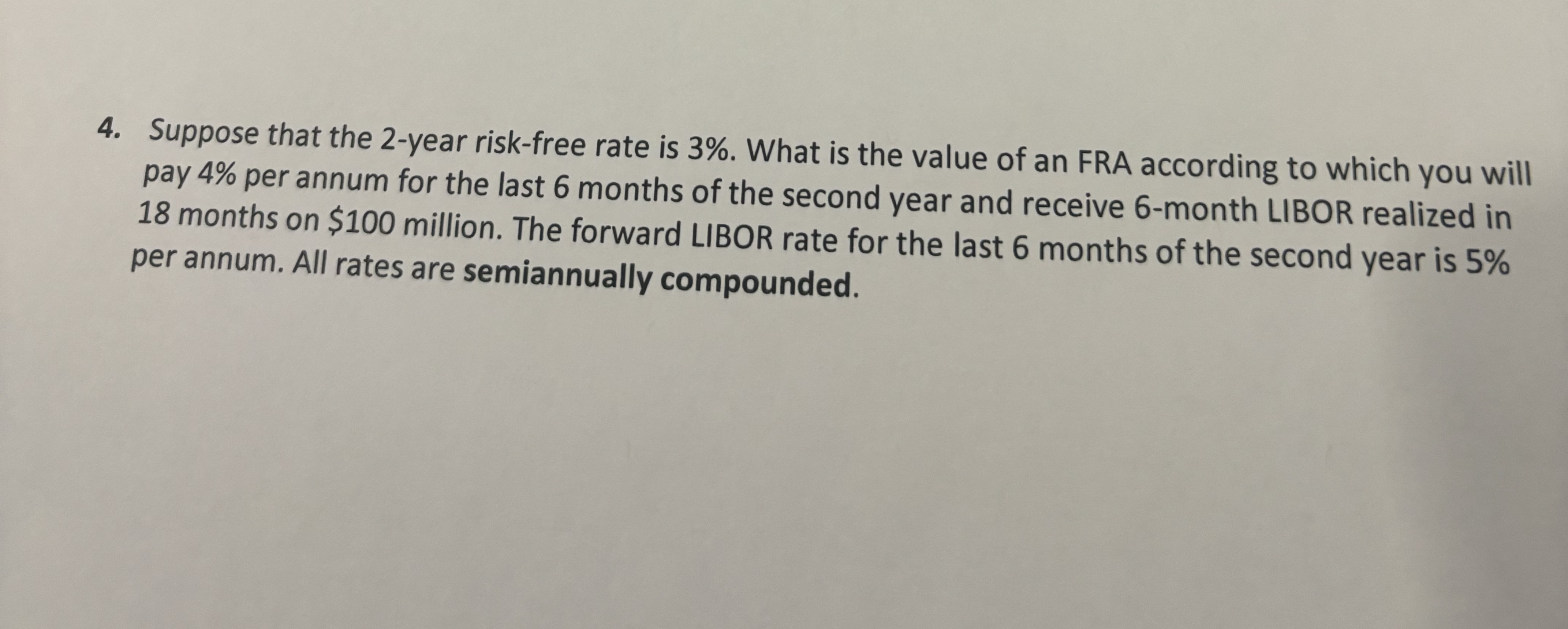

Suppose that the 2 - year risk - free rate is 3 % . What is the value of an FRA according to which you

Suppose that the year riskfree rate is What is the value of an FRA according to which you will pay per annum for the last months of the second year and receive month LIBOR realized in months on $ million. The forward LIBOR rate for the last months of the second year is per annum. All rates are semiannually compounded.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Emotions In Finance Booms Busts And Uncertainty

Authors: Jocelyn Pixley

2nd Edition

1107633370, 978-1107633377