Answered step by step

Verified Expert Solution

Question

1 Approved Answer

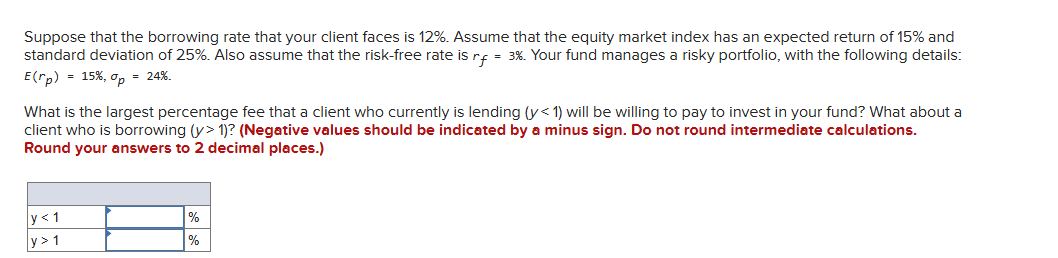

Suppose that the borrowing rate that your client faces is 12%. Assume that the equity market index has an expected return of 15% and

Suppose that the borrowing rate that your client faces is 12%. Assume that the equity market index has an expected return of 15% and standard deviation of 25%. Also assume that the risk-free rate is rf = 3%. Your fund manages a risky portfolio, with the following details: E(rp) = 15%, p = 24%. What is the largest percentage fee that a client who currently is lending (y < 1) will be willing to pay to invest in your fund? What about a client who is borrowing (y> 1)? (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.) y 1 % %

Step by Step Solution

★★★★★

3.45 Rating (168 Votes )

There are 3 Steps involved in it

Step: 1

Borrowing rate rf 12 Expected return of equity market index Erm 15 Standard deviation of equity mark...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus, Stylianos Perrakis, Peter

8th Canadian Edition

007133887X, 978-0071338875