Answered step by step

Verified Expert Solution

Question

1 Approved Answer

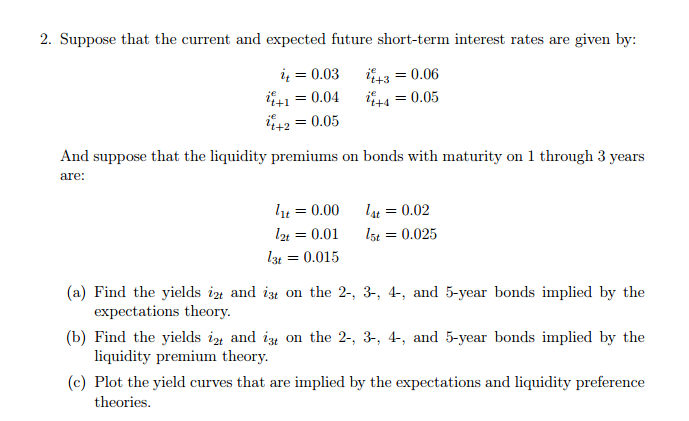

Suppose that the current and expected future short-term interest rates are given by: i_t = 0.03 i^e_t + 3 = 0.06 i^e_t + 1 =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Routledge Handbook Of Integrated Reporting

Authors: Charl De Villiers, Warren Maroun, Pei-Chi Hsiao

1st Edition

0367233851, 978-0367233853