Answered step by step

Verified Expert Solution

Question

1 Approved Answer

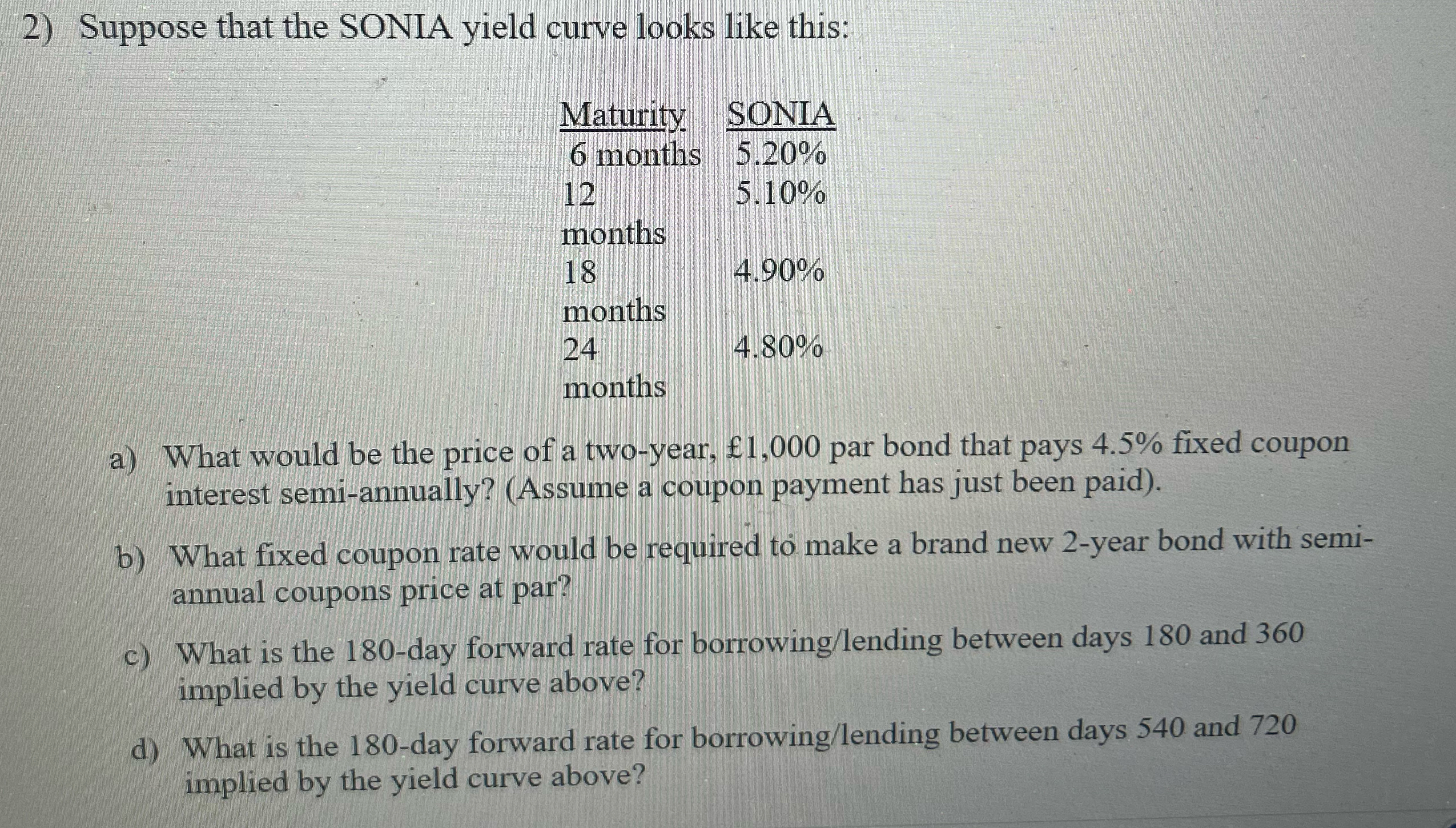

Suppose that the SONIA yield curve looks like this: table [ [ M a t u r i t y . 6 m o

Suppose that the SONIA yield curve looks like this:

tableSONJtablemonthstablemonth

a What would be the price of a twoyear, par bond that pays fixed coupon interest semiannually? Assume a coupon payment has just been paid

b What fixed coupon rate would be required t make a brand new year bond with semiannual coupons price at par?

c What is the day forward rate for borrowinglending between days and implied by the yield curve above?

d What is the day forward rate for borrowinglending between days and implied by the yield curve above?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Quantitative Finance

Authors: W.; T. Kleinkow; G. Stahl Hardle

1st Edition

3540434607, 978-3540434603