Answered step by step

Verified Expert Solution

Question

1 Approved Answer

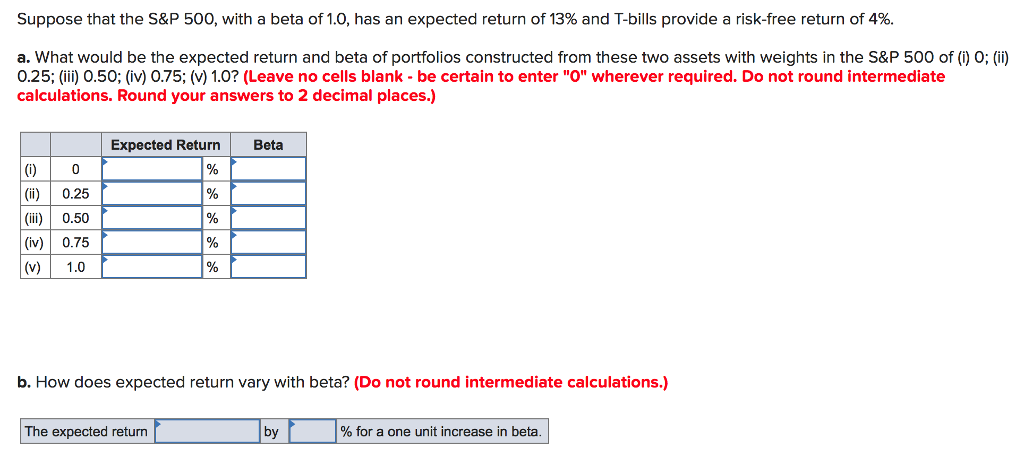

Suppose that the S&P 500, with a beta of 1.0, has an expected return of 13% and T-bills provide a risk-free return of 4%. a.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series Understanding Productivity Lessons From Longitudinal Microdata

Authors: United States Federal Reserve Board, Mark E. Doms, Eric J. Bartelsman

1st Edition

1288717261, 9781288717262