Answered step by step

Verified Expert Solution

Question

1 Approved Answer

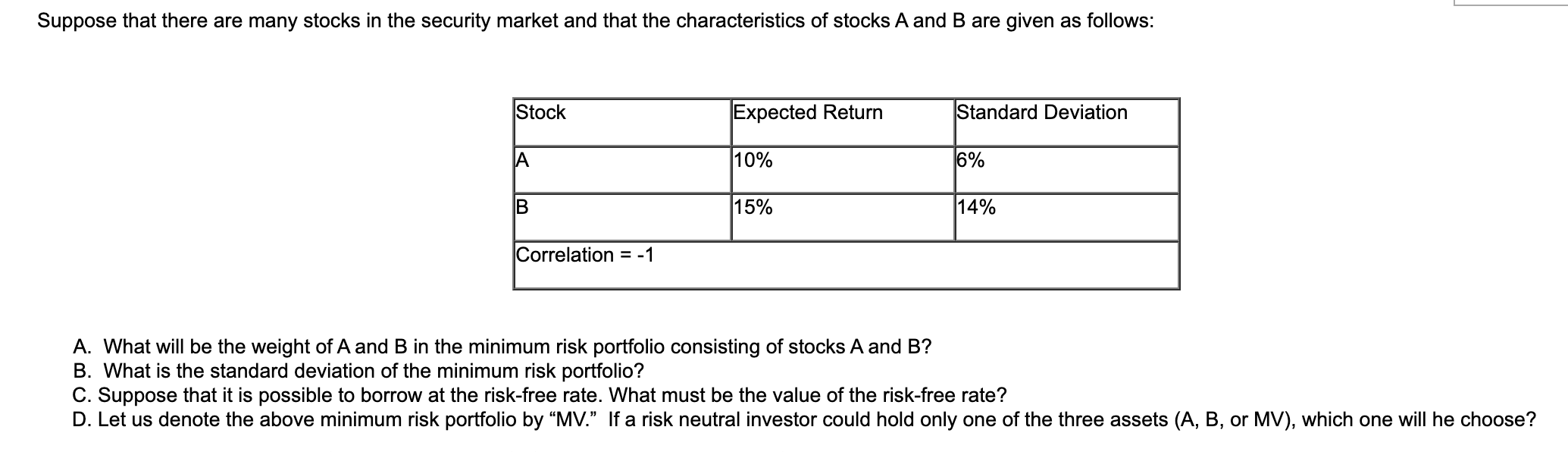

Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock

Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock A Expected Return 10% B 15% Correlation = -1 Standard Deviation 6% 14% A. What will be the weight of A and B in the minimum risk portfolio consisting of stocks A and B? B. What is the standard deviation of the minimum risk portfolio? C. Suppose that it is possible to borrow at the risk-free rate. What must be the value of the risk-free rate? D. Let us denote the above minimum risk portfolio by "MV." If a risk neutral investor could hold only one of the three assets (A, B, or MV), which one will he choose?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Non Financial Managers

Authors: Pierre Bergeron

7th edition

176530835, 978-0176530839