Answered step by step

Verified Expert Solution

Question

1 Approved Answer

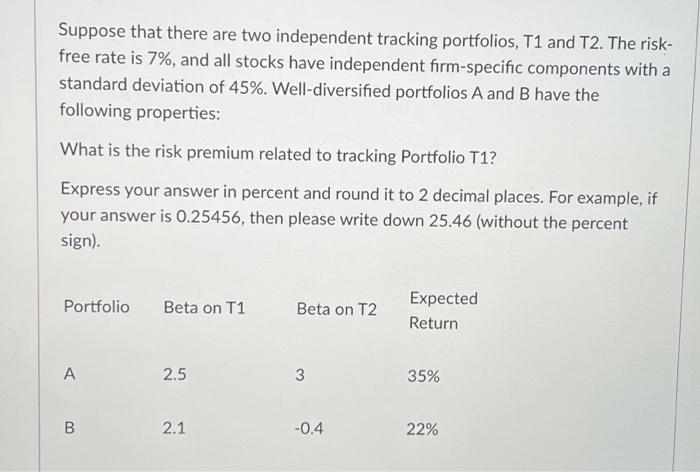

Suppose that there are two independent tracking portfolios, T1 and T2. The risk- free rate is 7%, and all stocks have independent firm-specific components with

Suppose that there are two independent tracking portfolios, T1 and T2. The risk- free rate is 7%, and all stocks have independent firm-specific components with a standard deviation of 45%. Well-diversified portfolios A and B have the following properties: What is the risk premium related to tracking Portfolio T1? Express your answer in percent and round it to 2 decimal places. For example, if your answer is 0.25456, then please write down 25.46 (without the percent sign). Portfolio Beta on T1 A B 2.5 2.1 Beta on T2 3 -0.4 Expected Return 35% 22%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Sterling Bonds And Fixed Income Handbook

Authors: Mark Glowrey

1st Edition

0857190423, 978-0857190420