Answered step by step

Verified Expert Solution

Question

1 Approved Answer

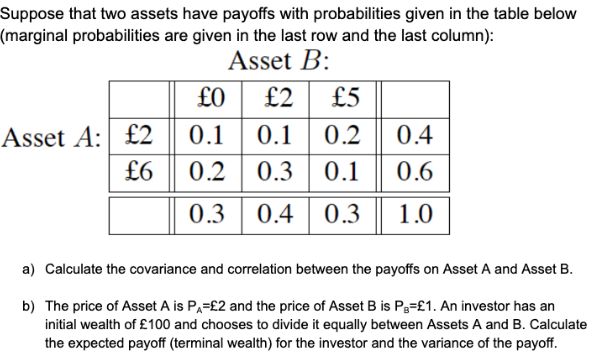

Suppose that two assets have payoffs with probabilities given in the table below (marginal probabilities are given in the last row and the last column):

Suppose that two assets have payoffs with probabilities given in the table below (marginal probabilities are given in the last row and the last column): Asset B : Asset A : a) Calculate the covariance and correlation between the payoffs on Asset A and Asset B. b) The price of Asset A is PA=2 and the price of Asset B is PB=1. An investor has an initial wealth of 100 and chooses to divide it equally between Assets A and B. Calculate the expected payoff (terminal wealth) for the investor and the variance of the payoff

Suppose that two assets have payoffs with probabilities given in the table below (marginal probabilities are given in the last row and the last column): Asset B : Asset A : a) Calculate the covariance and correlation between the payoffs on Asset A and Asset B. b) The price of Asset A is PA=2 and the price of Asset B is PB=1. An investor has an initial wealth of 100 and chooses to divide it equally between Assets A and B. Calculate the expected payoff (terminal wealth) for the investor and the variance of the payoff Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: E. Thomas Garman, Raymond E. Forgue, Jonathan Fox

14th Edition

0357901495, 9780357901496