Answered step by step

Verified Expert Solution

Question

1 Approved Answer

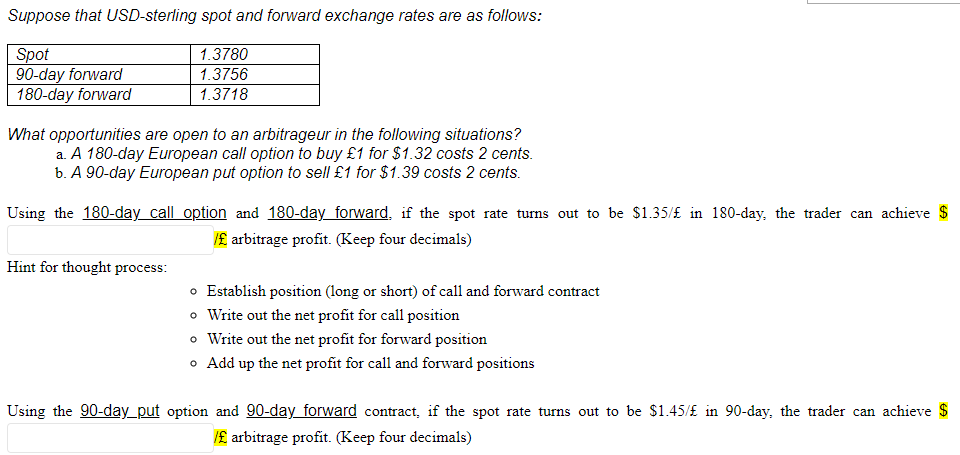

Suppose that USD-sterling spot and forward exchange rates are as follows: What opportunities are open to an arbitrageur in the following situations? a. A 180-day

Suppose that USD-sterling spot and forward exchange rates are as follows: What opportunities are open to an arbitrageur in the following situations? a. A 180-day European call option to buy 1 for $1.32 costs 2 cents. b. A 90-day European put option to sell 1 for $1.39 costs 2 cents. Using the 180-day call option and 180-day forward, if the spot rate turns out to be $1.35/ in 180 -day, the trader can achieve $ E arbitrage profit. (Keep four decimals) Hint for thought process: - Establish position (long or short) of call and forward contract - Write out the net profit for call position - Write out the net profit for forward position - Add up the net profit for call and forward positions Using the 90-day_put option and 90-day forward contract, if the spot rate turns out to be $1.45/ in 90 -day, the trader can achieve $ arbitrage profit. (Keep four decimals)

Suppose that USD-sterling spot and forward exchange rates are as follows: What opportunities are open to an arbitrageur in the following situations? a. A 180-day European call option to buy 1 for $1.32 costs 2 cents. b. A 90-day European put option to sell 1 for $1.39 costs 2 cents. Using the 180-day call option and 180-day forward, if the spot rate turns out to be $1.35/ in 180 -day, the trader can achieve $ E arbitrage profit. (Keep four decimals) Hint for thought process: - Establish position (long or short) of call and forward contract - Write out the net profit for call position - Write out the net profit for forward position - Add up the net profit for call and forward positions Using the 90-day_put option and 90-day forward contract, if the spot rate turns out to be $1.45/ in 90 -day, the trader can achieve $ arbitrage profit. (Keep four decimals) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modeling Financial Time Series With S PLUS

Authors: Eric Zivot, Jiahui Wang

2nd Edition

0387279652, 0387323481, 9780387279657, 9780387323480