Question

Suppose that you go short two contracts of April platinum futures on January 20 and long three contracts of June gold on January 21. Then

Suppose that you go short two contracts of April platinum futures on January 20 and long three contracts of June gold on January 21. Then how much the value of your portfolio at the closing of January 22 has changed by?

(5 marks)

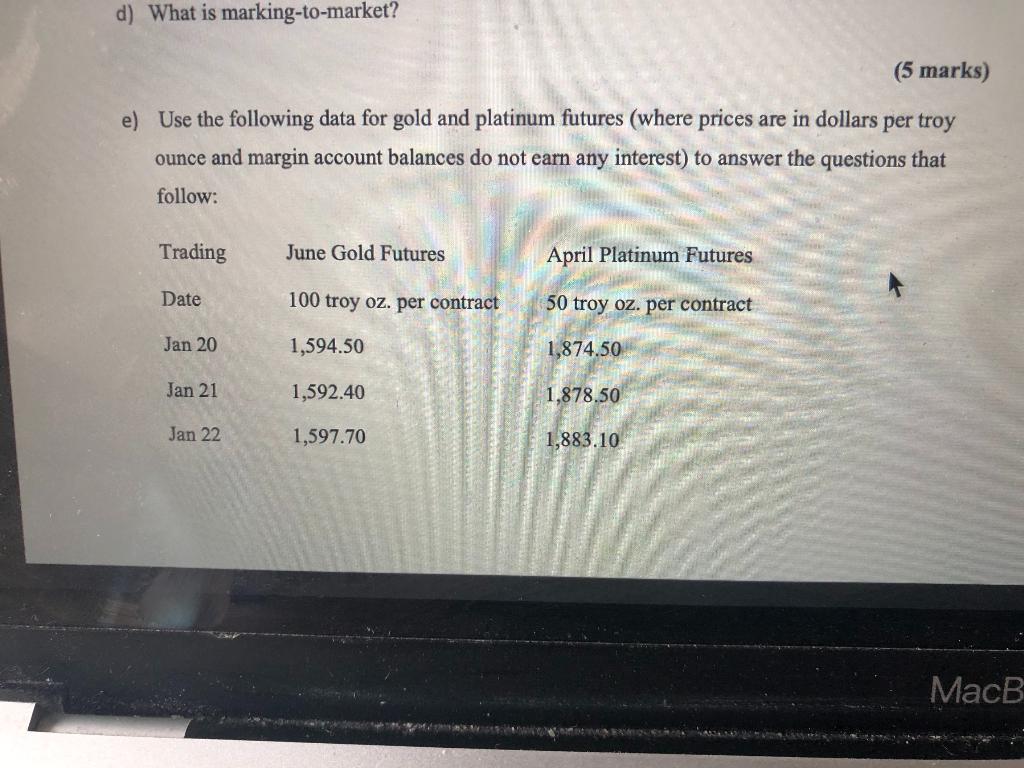

d) What is marking-to-market? (5 marks) e) Use the following data for gold and platinum futures (where prices are in dollars per troy ounce and margin account balances do not earn any interest) to answer the questions that follow: Trading June Gold Futures April Platinum Futures Date 100 troy oz. per contract 50 troy oz. per contract Jan 20 1,594.50 1,874.50 Jan 21 1,592.40 1,878.50 Jan 22 1,597.70 1,883.10 MacB d) What is marking-to-market? (5 marks) e) Use the following data for gold and platinum futures (where prices are in dollars per troy ounce and margin account balances do not earn any interest) to answer the questions that follow: Trading June Gold Futures April Platinum Futures Date 100 troy oz. per contract 50 troy oz. per contract Jan 20 1,594.50 1,874.50 Jan 21 1,592.40 1,878.50 Jan 22 1,597.70 1,883.10 MacBStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley B. Block, Geoffrey A. Hirt, Bartley R. Danielsen

13th Edition

0073382388, 978-0073382388