Question

Suppose the risk-free rate is 6%. Also assume the expected return equals to average return for each stock. Calculate 1) the weights for the two

Suppose the risk-free rate is 6%. Also assume the expected return equals to average return for each stock. Calculate 1) the weights for the two stocks in the optimal risky portfolio; 2) the return and risk (standard deviation) of the portfolio.

Suppose the risk-free rate is 6%. Also assume the expected return equals to average return for each stock. Calculate 1) the weights for the two stocks in the optimal risky portfolio; 2) the return and risk (standard deviation) of the portfolio.

If a client demands a $100,000 complete portfolio with an expected return of 25%. Use information and your answer above. Find the amount of money invested in stocks ABC and XYZ, and the risk-free asset.

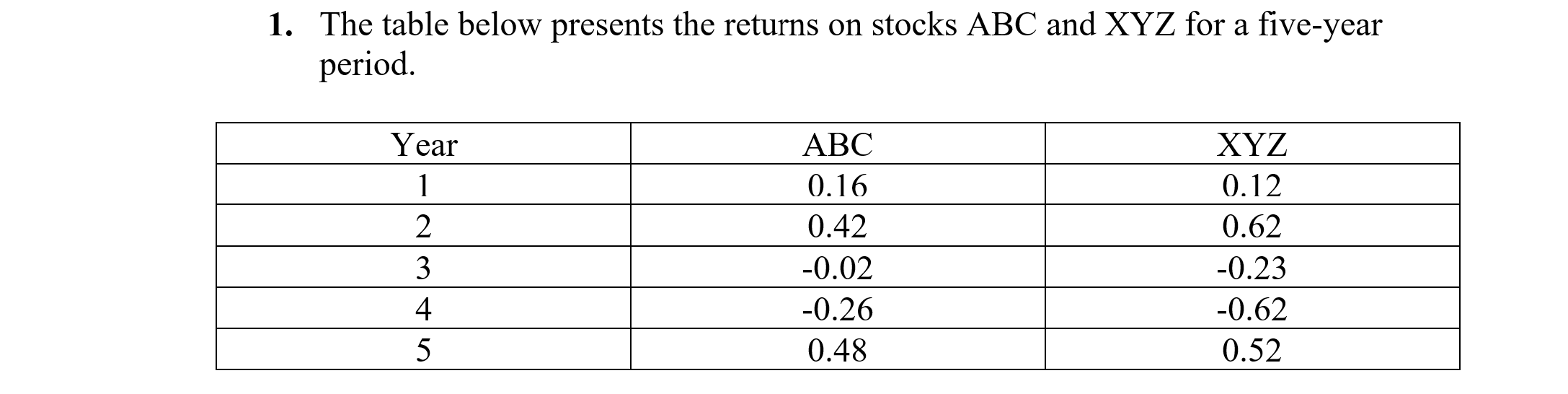

1. The table below presents the returns on stocks ABC and XYZ for a five-year period. Year 1 2 ABC 0.16 0.42 -0.02 -0.26 0.48 XYZ 0.12 0.62 -0.23 -0.62 0.52 3 4 5 1. The table below presents the returns on stocks ABC and XYZ for a five-year period. Year 1 2 ABC 0.16 0.42 -0.02 -0.26 0.48 XYZ 0.12 0.62 -0.23 -0.62 0.52 3 4 5Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Futures And Options Markets

Authors: John Hull

9th Global Edition

1292422114, 9781292422114