Answered step by step

Verified Expert Solution

Question

1 Approved Answer

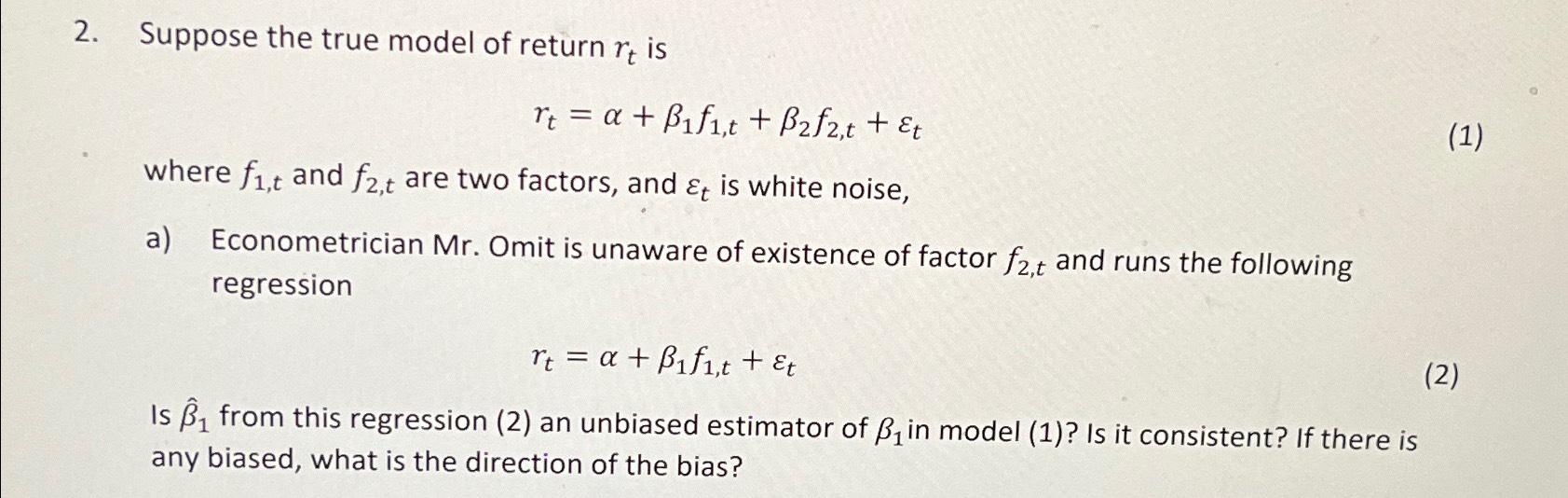

Suppose the true model of return r t is r t = + 1 f 1 , t + 2 f 2 , t +

Suppose the true model of return is

where and are two factors, and is white noise,

a Econometrician Mr Omit is unaware of existence of factor and runs the following regression

Is hat from this regression an unbiased estimator of in model Is it consistent? If there is any biased, what is the direction of the bias?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

High School Math 2012 Common-core Algebra 2 Grade 10/11

Authors: Savvas Learning Co

Student Edition

9780133186024, 0133186024