Answered step by step

Verified Expert Solution

Question

1 Approved Answer

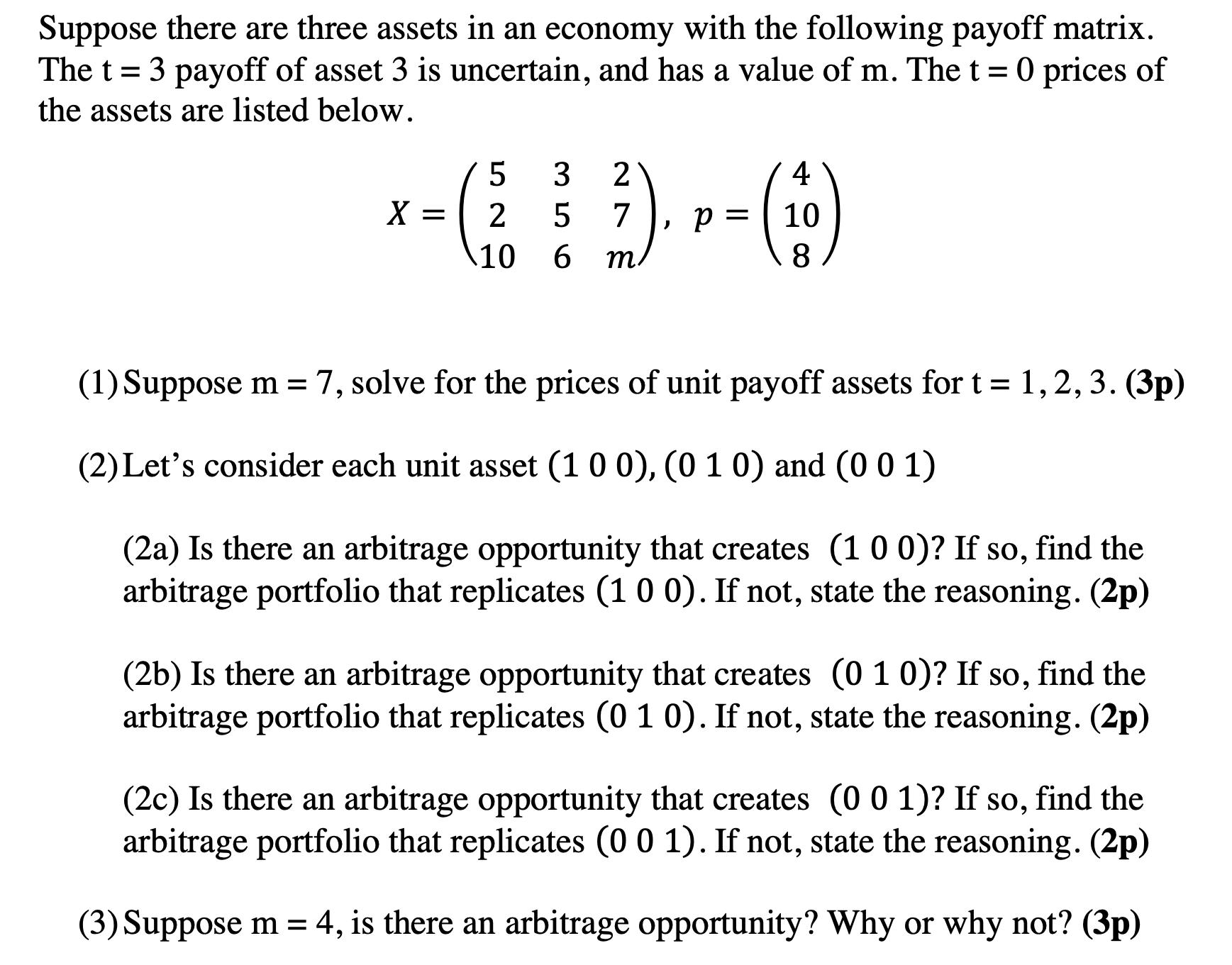

Suppose there are three assets in an economy with the following payoff matrix. The t = 3 payoff of asset 3 is uncertain, and

Suppose there are three assets in an economy with the following payoff matrix. The t = 3 payoff of asset 3 is uncertain, and has a value of m. The t = 0 prices of the assets are listed below. 5 = ( X = 3 2 7 2 5 10 6 m. 4 = (0) 10 8 , p = (1) Suppose m = 7, solve for the prices of unit payoff assets for t = 1, 2, 3. (3p) (2) Let's consider each unit asset (1 0 0), (010) and (001) (2a) Is there an arbitrage opportunity that creates (100)? If so, find the arbitrage portfolio that replicates (1 0 0). If not, state the reasoning. (2p) (2b) Is there an arbitrage opportunity that creates (010)? If so, find the arbitrage portfolio that replicates (0 1 0). If not, state the reasoning. (2p) (2c) Is there an arbitrage opportunity that creates (0 0 1)? If so, find the arbitrage portfolio that replicates (0 0 1). If not, state the reasoning. (2p) (3) Suppose m = 4, is there an arbitrage opportunity? Why or why not? (3p)

Step by Step Solution

★★★★★

3.48 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

1 Given that m 7 we can solve for the prices of unit payoff assets for t 1 2 and 3 based on the prov...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus

Authors: Ron Larson, Bruce H. Edwards

10th Edition

1285057090, 978-1285057095