Answered step by step

Verified Expert Solution

Question

1 Approved Answer

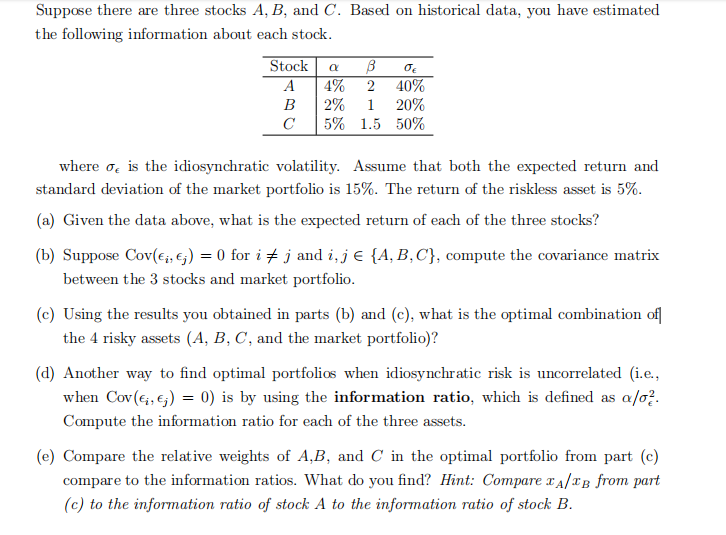

Suppose there are three stocks A,B, and C. Based on historical data, you have estimated the following information about each stock. where is the idiosynchratic

Suppose there are three stocks A,B, and C. Based on historical data, you have estimated the following information about each stock. where is the idiosynchratic volatility. Assume that both the expected return and standard deviation of the market portfolio is 15%. The return of the riskless asset is 5%. (a) Given the data above, what is the expected return of each of the three stocks? (b) Suppose Cov(i,j)=0 for i=j and i,j{A,B,C}, compute the covariance matrix between the 3 stocks and market portfolio. (c) Using the results you obtained in parts (b) and (c), what is the optimal combination of the 4 risky assets ( A,B,C, and the market portfolio)? (d) Another way to find optimal portfolios when idiosynchratic risk is uncorrelated (i.e., when Cov(i,j)=0) is by using the information ratio, which is defined as /2. Compute the information ratio for each of the three assets. (e) Compare the relative weights of A,B, and C in the optimal portfolio from part (c) compare to the information ratios. What do you find? Hint: Compare xA/xB from part (c) to the information ratio of stock A to the information ratio of stock B. (f) Redo your answers to part (a) and (c) under the assumption that the CAPMinolds (i.e., assume that =0 for all stocks). Hint: No calculation is necessary to redo part (c)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started