Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Suppose you are given the following information about the default-free, coupon-paying yield curve: Mat Cou YTN a. Use arbitrage to determine the yield to maturity

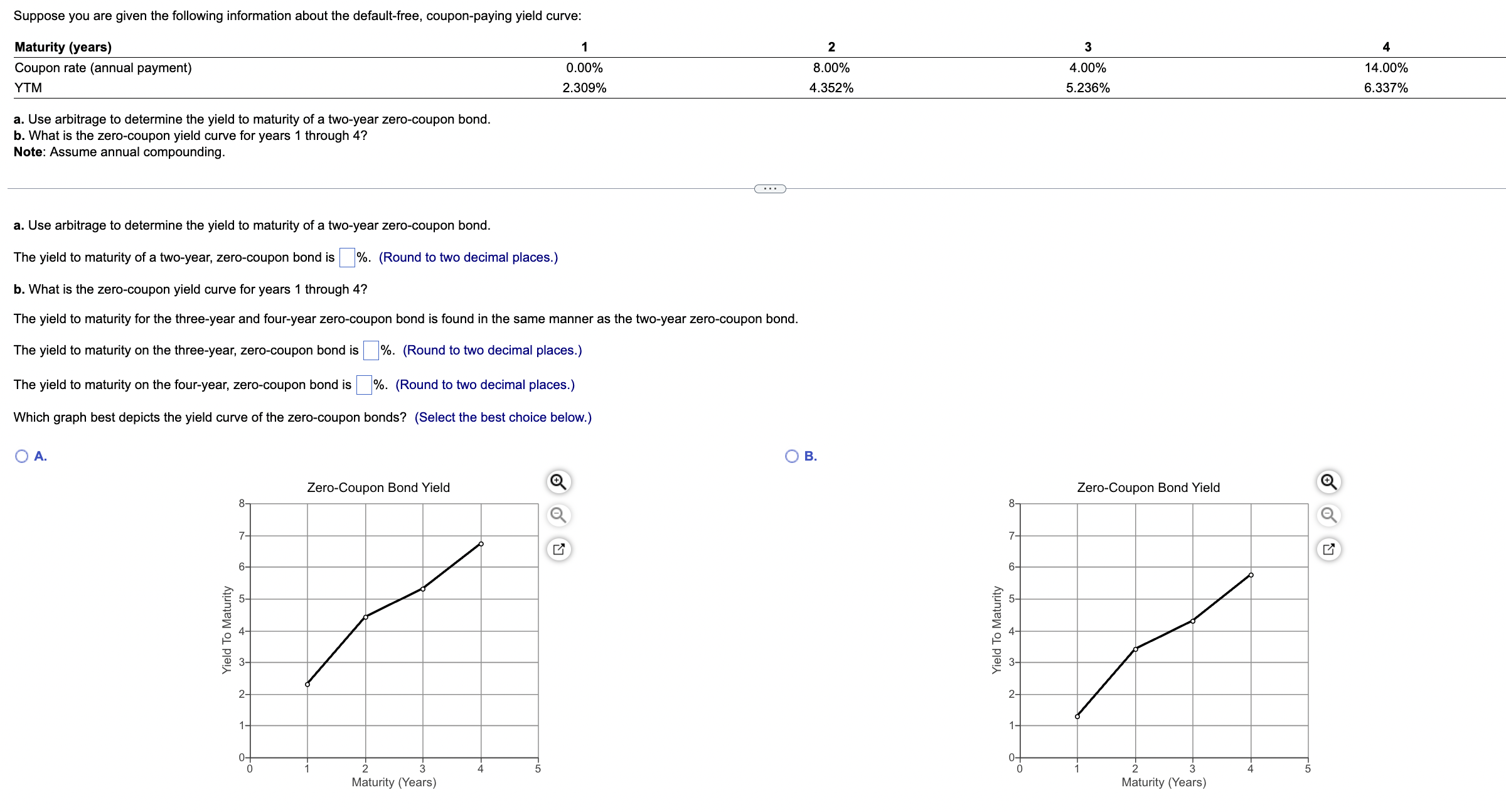

Suppose you are given the following information about the default-free, coupon-paying yield curve: Mat Cou YTN a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4 ? Note: Assume annual compounding. a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. The yield to maturity of a two-year, zero-coupon bond is o. (Round to two decimal places.) b. What is the zero-coupon yield curve for years 1 through 4 ? The yield to maturity for the three-year and four-year zero-coupon bond is found in the same manner as the two-year zero-coupon bond. The yield to maturity on the three-year, zero-coupon bond i: \%. (Round to two decimal places.) The yield to maturity on the four-year, zero-coupon bond is '. (Round to two decimal places.) Which graph best depicts the yield curve of the zero-coupon bonds? (Select the best choice below.)

Suppose you are given the following information about the default-free, coupon-paying yield curve: Mat Cou YTN a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4 ? Note: Assume annual compounding. a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. The yield to maturity of a two-year, zero-coupon bond is o. (Round to two decimal places.) b. What is the zero-coupon yield curve for years 1 through 4 ? The yield to maturity for the three-year and four-year zero-coupon bond is found in the same manner as the two-year zero-coupon bond. The yield to maturity on the three-year, zero-coupon bond i: \%. (Round to two decimal places.) The yield to maturity on the four-year, zero-coupon bond is '. (Round to two decimal places.) Which graph best depicts the yield curve of the zero-coupon bonds? (Select the best choice below.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Asset And Liability Management Volume 2

Authors: S. A. Zenios, W. T. Ziemba

1st Edition

0444528024, 978-0444528025