Answered step by step

Verified Expert Solution

Question

1 Approved Answer

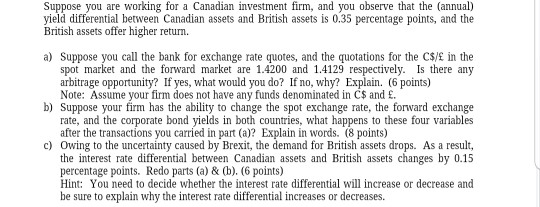

Suppose you are working for a Canadian investment firm, and you observe that the (annual) yield differential between Canadian assets and British assets is 0.35

Suppose you are working for a Canadian investment firm, and you observe that the (annual) yield differential between Canadian assets and British assets is 0.35 percentage points, and the British assets offer higher return a) Suppose you call the bank for exchange rate quotes, and the quotations for the C$/E in the spot market and the forward market are 1.4200 and 1.4129 respectively. Is there any arbitrage opportunity? If yes, what would you do? If no, why? Explain. (6 points) Note: Assume your firm does not have any funds denominated in CS and . b) Suppose your firm has the ability to change the spot exchange rate, the forward exchange rate, and the corporate bond yields in both countries, what happens to these four variables after the transactions you carried in part (a)? Explain in words. (8 points) c) Owing to the uncertainty caused by Brexit, the demand for British assets drops. As a result, the interest rate differential between Canadian assets and British assets changes by 0.15 percentage points. Redo parts (a) & (b). (6 points) Hint: You need to decide whether the interest rate differential will increase or decrease and be sure to explain why the interest rate differential increases or decreases. Suppose you are working for a Canadian investment firm, and you observe that the (annual) yield differential between Canadian assets and British assets is 0.35 percentage points, and the British assets offer higher return a) Suppose you call the bank for exchange rate quotes, and the quotations for the C$/E in the spot market and the forward market are 1.4200 and 1.4129 respectively. Is there any arbitrage opportunity? If yes, what would you do? If no, why? Explain. (6 points) Note: Assume your firm does not have any funds denominated in CS and . b) Suppose your firm has the ability to change the spot exchange rate, the forward exchange rate, and the corporate bond yields in both countries, what happens to these four variables after the transactions you carried in part (a)? Explain in words. (8 points) c) Owing to the uncertainty caused by Brexit, the demand for British assets drops. As a result, the interest rate differential between Canadian assets and British assets changes by 0.15 percentage points. Redo parts (a) & (b). (6 points) Hint: You need to decide whether the interest rate differential will increase or decrease and be sure to explain why the interest rate differential increases or decreases

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance Essentials Saving And Investing

Authors: Julia A Heath

1st Edition

1604139897, 9781604139891