Answered step by step

Verified Expert Solution

Question

1 Approved Answer

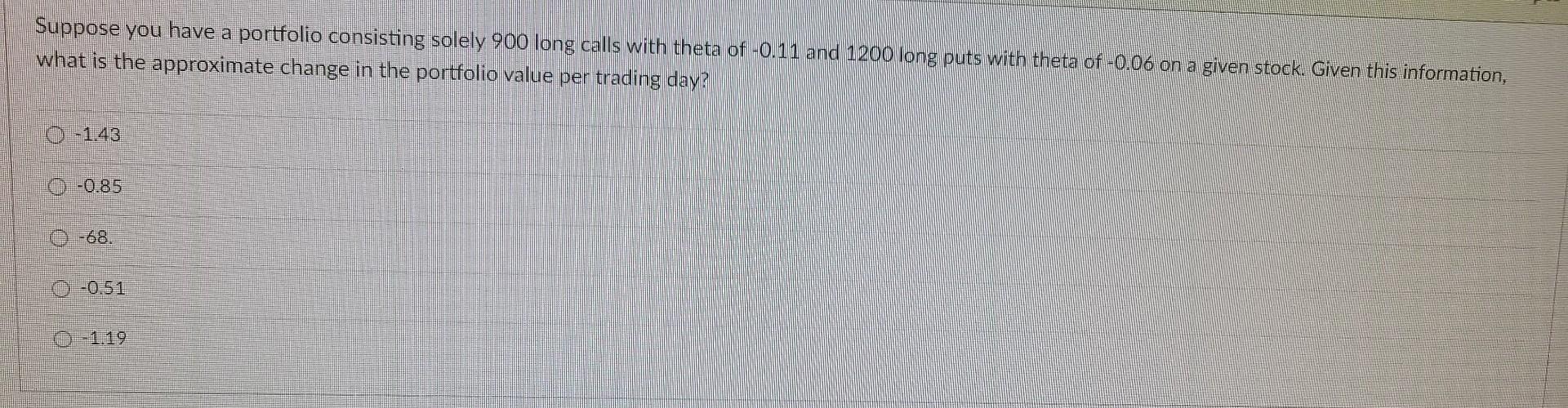

Suppose you have a portfolio consisting solely 900 long calls with theta of - 0.11 and 1200 long puts with theta of - 0.06 on

Suppose you have a portfolio consisting solely 900 long calls with theta of - 0.11 and 1200 long puts with theta of - 0.06 on a given stock. Given this information, What is the approximate change in the portfolio value per trading day? 1.43 0.85 68. 0.51 1.19

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Blockchain The Main Concepts Of Blockchains Bitcoin And Cryptocurrencies

Authors: Norman Guagliano

1st Edition

979-8354135547