Answered step by step

Verified Expert Solution

Question

1 Approved Answer

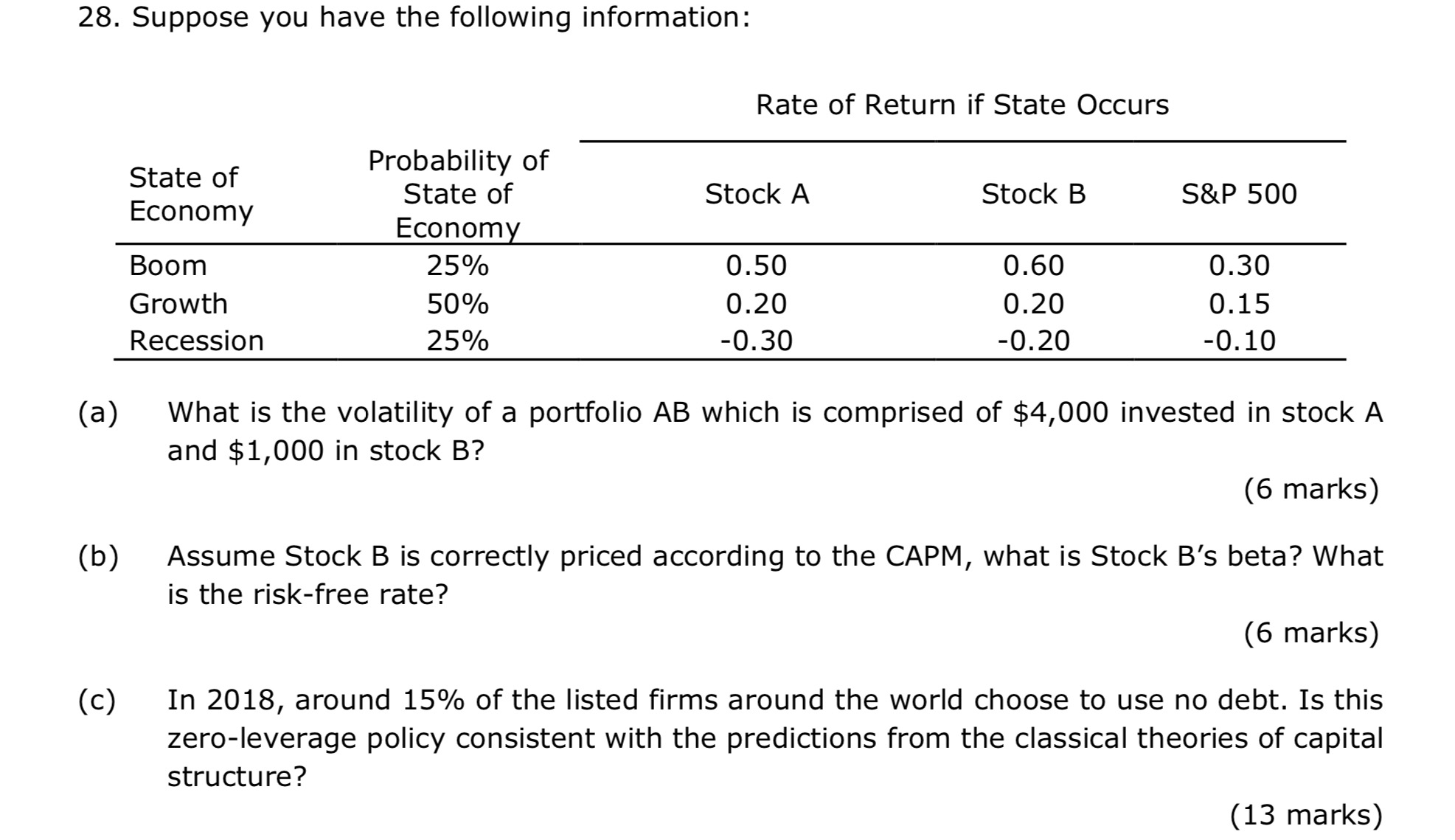

Suppose you have the following information: ( a ) What is the volatility of a portfolio A B which is comprised of $ 4 ,

Suppose you have the following information:

a What is the volatility of a portfolio which is comprised of $ invested in stock

and $ in stock

marks

b Assume Stock B is correctly priced according to the CAPM, what is Stock Bs beta? What

is the riskfree rate?

marks

c In around of the listed firms around the world choose to use no debt. Is this

zeroleverage policy consistent with the predictions from the classical theories of capital

structure?

marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cybersecurity In Finance

Authors: Sylvain Bouyon, Simon Krause

1st Edition

1786612178, 9781786612175