Answered step by step

Verified Expert Solution

Question

1 Approved Answer

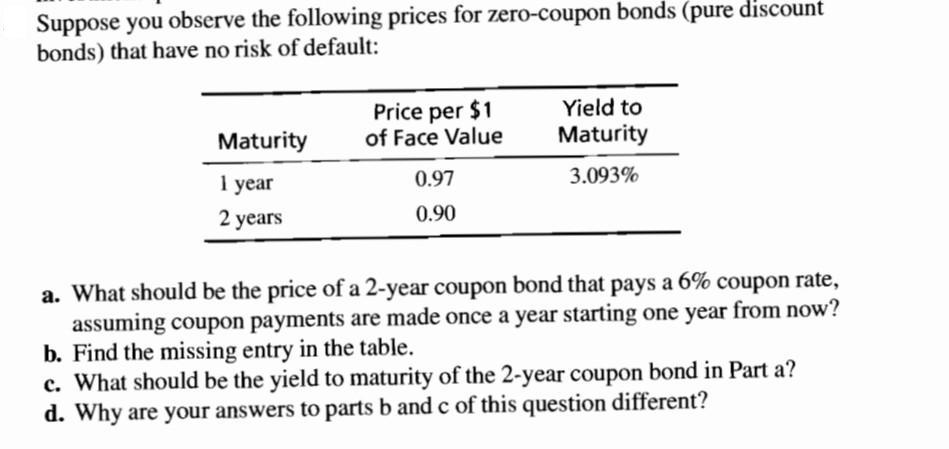

Suppose you observe the following prices for zero-coupon bonds (pure discount bonds) that have no risk of default: Maturity 1 year 2 years Price

Suppose you observe the following prices for zero-coupon bonds (pure discount bonds) that have no risk of default: Maturity 1 year 2 years Price per $1 of Face Value 0.97 0.90 Yield to Maturity 3.093% a. What should be the price of a 2-year coupon bond that pays a 6% coupon rate, assuming coupon payments are made once a year starting one year from now? b. Find the missing entry in the table. c. What should be the yield to maturity of the 2-year coupon bond in Part a? d. Why are your answers to parts b and c of this question different?

Step by Step Solution

★★★★★

3.52 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

a Present value of first years cash flow 6 x 97 582 Present value of second years cash flow 106 x...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Corporate Finance

Authors: Laurence Booth, Sean Cleary

3rd Edition

978-1118300763, 1118300769