Answered step by step

Verified Expert Solution

Question

1 Approved Answer

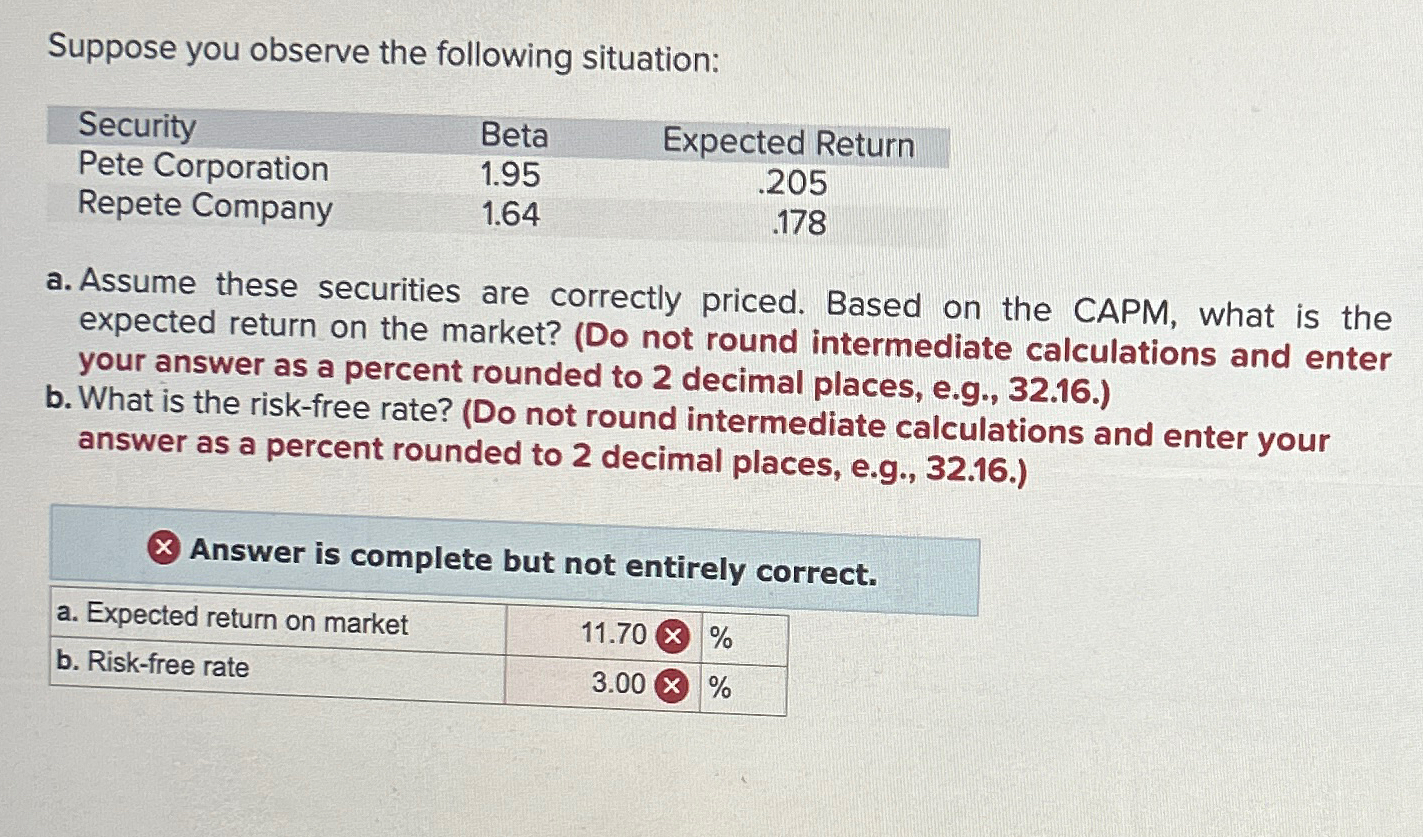

Suppose you observe the following situation: table [ [ Security , Beta,Expected Return ] , [ Pete Corporation, 1 . 9 5 , .

Suppose you observe the following situation:

tableSecurityBeta,Expected ReturnPete Corporation,Repete Company,

a Assume these securities are correctly priced. Based on the CAPM, what is the expected return on the market? Do not round intermediate calculations and enter your answer as a percent rounded to decimal places, eg

b What is the riskfree rate? Do not round intermediate calculations and enter your answer as a percent rounded to decimal places, eg

Answer is complete but not entirely correct.

tablea Expected return on market,b Riskfree rate,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Campaign Finance

Authors: Robert E. Mutch

1st Edition

0190274697, 9780190274696