Answered step by step

Verified Expert Solution

Question

1 Approved Answer

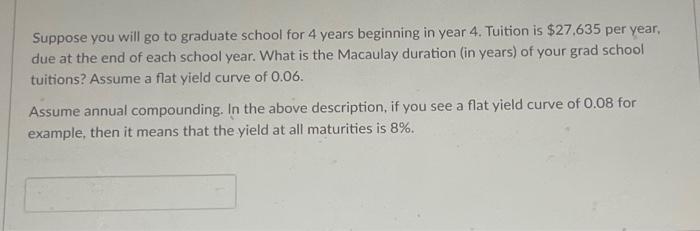

Suppose you will go to graduate school for 4 years beginning in year 4 . Tuition is $27.635 per year. due at the end of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Which Crypto Currency Should I Buy Make Finding And Investing In New Crypto Currencies Fun Easy And Profitable

Authors: Lisa Phillips

1st Edition

1732644586, 978-1732644588