Answered step by step

Verified Expert Solution

Question

1 Approved Answer

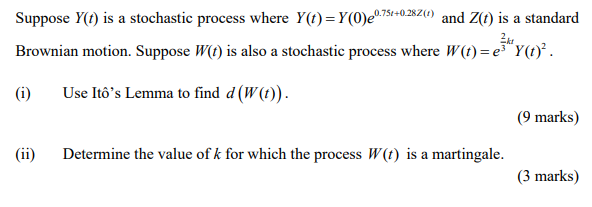

Suppose Y(t) is a stochastic process where Y(t)=Y(0)e0.75t+0.28Z(t) and Z(t) is a standard Brownian motion. Suppose W(t) is also a stochastic process where W(t)=e32ktY(t)2. (i)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Moorad Choudhry Anthology Website Past Present And Future Principles Of Banking And Finance

Authors: Moorad Choudhry

1st Edition

1118779738, 978-1118779736