Answered step by step

Verified Expert Solution

Question

1 Approved Answer

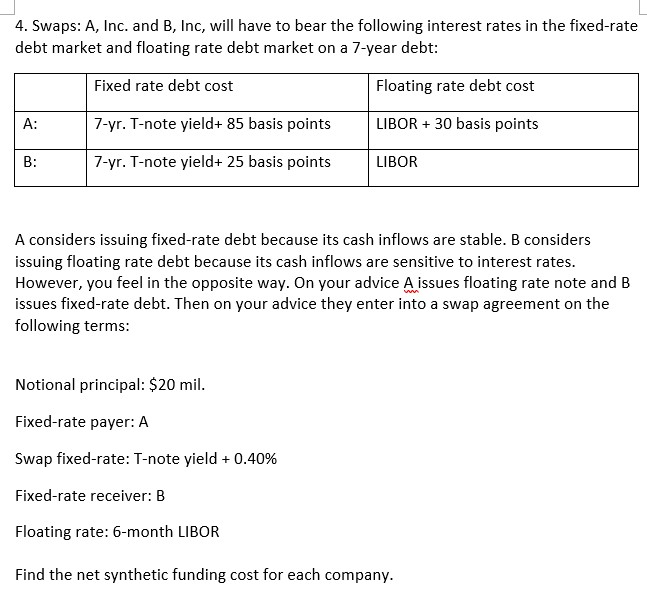

SWAPS 4. Swaps: A, Inc. and B, Inc, will have to bear the following interest rates in the fixed-rate debt market and floating rate debt

SWAPS

4. Swaps: A, Inc. and B, Inc, will have to bear the following interest rates in the fixed-rate debt market and floating rate debt market on a 7-year debt: Fixed rate debt cost 7-yr. T-note yield+ 85 basis points LIBOR 30 basis points 7-yr. T-note yield+ 25 basis points LIBOR Floating rate debt cost A: B: A considers issuing fixed-rate debt because its cash inflows are stable. B considers issuing floating rate debt because its cash inflows are sensitive to interest rates. However, you feel in the opposite way. On your advice A issues floating rate note and B issues fixed-rate debt. Then on your advice they enter into a swap agreement on the following terms: Notional principal: $20 mil Fixed-rate payer: A Swap fixed-rate: T-note yield + 0.40% Fixed-rate receiver: B Floating rate: 6-month LIBOR Find the net synthetic funding cost for each company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Finance Theory And Practice

Authors: Terrence M. Clauretie, G. Stacy Sirmans

4th Edition

032414377X, 978-0324143775