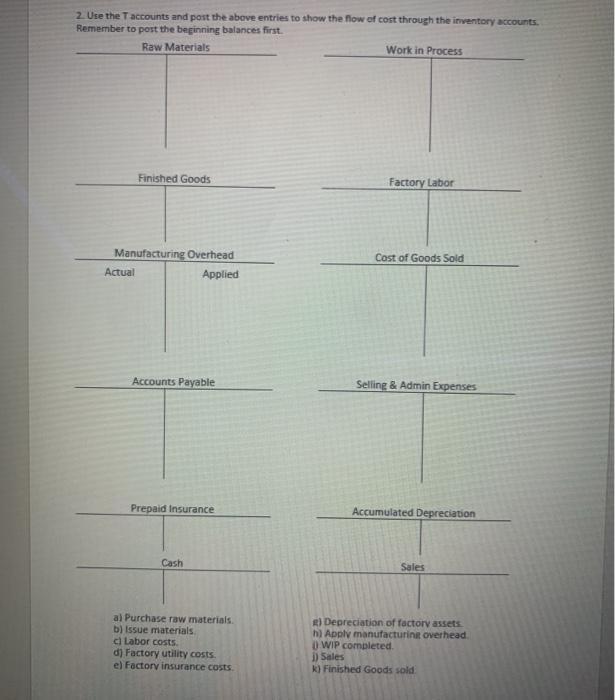

T accounts please

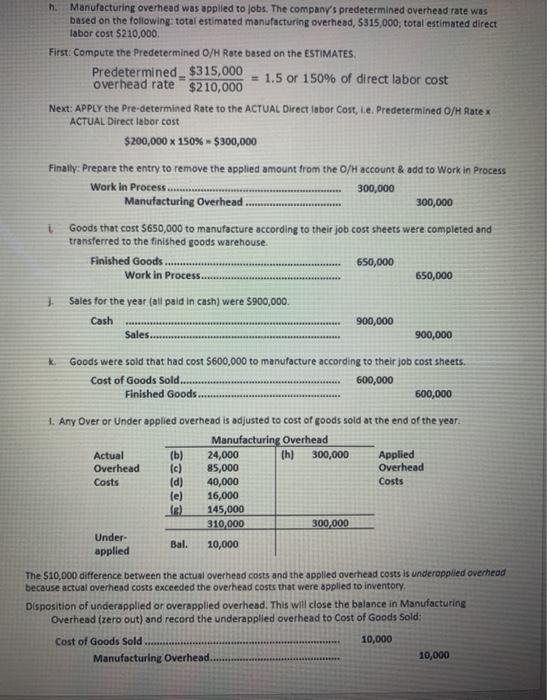

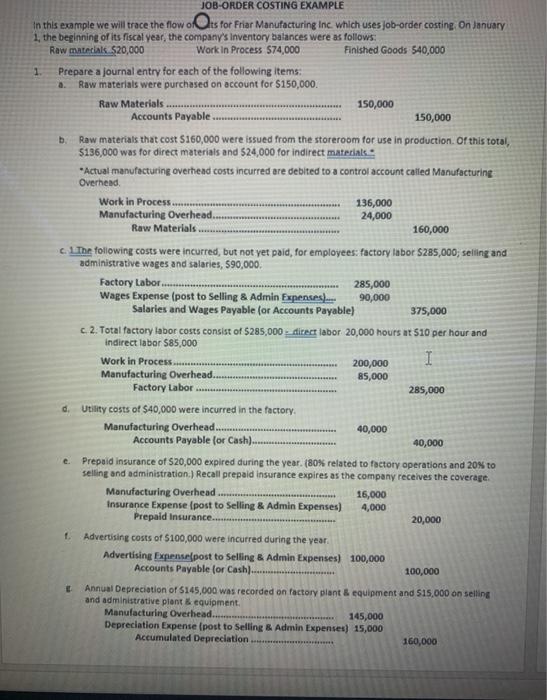

JOB-ORDER COSTING EXAMPLE In this example we will trace the flow ots for Friar Manufacturing Inc which uses Job-order costing. On January 1, the beginning of its fiscal year, the company's Inventory balances were as follows: Raw materials 520,000 Work in Process 574,000 Finished Goods 540,000 1 Prepare a journal entry for each of the following items Raw materials were purchased on account for $150,000. Raw Materials 150,000 Accounts Payable 150,000 b. Raw materials that cost $160,000 were issued from the storeroom for use in production. Of this total, 5136,000 was for direct materials and $24,000 for indirect materials, Actual manufacturing overhead costs incurred are debited to a control account called Manufacturing Overhead Work in Process... 136,000 Manufacturing Overhead... 24,000 Raw Materials 160,000 che following costs were incurred, but not yet paid, for employees: factory labor $285,000; seling and administrative wages and salaries, 590,000 Factory Labor. 285,000 Wages Expense (post to Selling & Admin Expenses.... 90,000 Salaries and Wages Payable for Accounts Payable) 375,000 c. 2. Total factory labor costs consist of $285,000 - direct labor 20,000 hours at 510 per hour and Indirect labor $85,000 Work in Process 200,000 I Manufacturing Overhead.. 85,000 Factory Labor 285,000 Utility costs of $40,000 were incurred in the factory Manufacturing Overhead ...... 40,000 Accounts Payable for Cash). 40,000 Prepaid insurance of S20,000 expired during the year. (80% related to factory operations and 20% to selling and administration.) Recall prepaid insurance expires as the company receives the coverage Manufacturing Overhead 16,000 Insurance Expense (post to Selling & Admin Expenses) 4,000 Prepaid Insurance... 20,000 Advertising costs of $100,000 were incurred during the year Advertising Expense post to Selling & Admin Expenses) 100,000 Accounts Payable (or Cash). 100,000 Annual Depreciation of 145,000 was recorded on factory plant & equipment and 515,000 on selling and administrative plant & equipment Manufacturing Overhead..... 145,000 Depreciation Expense (post to Selling & Admin Expenses) 15,000 Accumulated Depreciation 160,000 d f E h Manufacturing overhead was applied to jobs. The company's predetermined overhead rate was based on the following total estimated manufacturing overhead, 5315,000, total estimated direct labor cost $210,000 First: Compute the predetermined O/H Rate based on the ESTIMATES Predetermined $315,000 overhead rate $210,000 = 1.5 or 150% of direct labor cost Next: APPLY the Pre-determined Rate to the ACTUAL Direct labor Cost, Le Predetermined O/H Ratex ACTUAL Direct labor cost $200,000 x 150% - $300,000 Finally: Prepare the entry to remove the applied amount from the O/H account & add to Work in Process Work in Process 300,000 Manufacturing Overhead 300,000 Goods that cost $650,000 to manufacture according to their job cost sheets were completed and transferred to the finished goods warehouse. Finished Goods 650,000 Work in Process. 650,000 1 Sales for the year (all peld in cash) were $900,000. Cash 900,000 Sales. 900,000 Goods were sold that had cost $600,000 to manufacture according to their job cost sheets. Cost of Goods Sold......... 600,000 Finished Goods. 600,000 1. Any Over or Under applied overhead is adjusted to cost of goods sold at the end of the year. Manufacturing Overhead Actual (b) 24,000 (h) 300,000 Applied Overhead (c) 85,000 Overhead Costs (d) 40,000 Costs le) 16,000 1) 145,000 310,000 300,000 Under Bal. 10,000 applied The 510,000 difference between the actual overhead costs and the applied overhead costs is underopplied overhead because actual overhead costs exceeded the overhead costs that were applied to inventory Disposition of underapplied or overapplied overhead. This will close the balance in Manufacturing Overhead (zero out) and record the underapplied overhead to Cost of Goods Sold: Cost of Goods Sold 10,000 Manufacturing Overhead. 10,000 2. Use the accounts and post the above entries to show the flow of cost through the inventory accounts. Remember to post the beginning balances first. Raw Materials Work in Process Finished Goods Factory Labor Cost of Goods Sold Manufacturing Overhead Actual Applied Accounts Payable Selling & Admin Expenses Prepaid Insurance Accumulated Depreciation Cash Sales al Purchase raw materials b) Issue materials ci Labor costs d) Factory utility costs e) Factory insurance costs ) Depreciation of factory assets h) Apply manufacturing overhead O WIP completed 1) Sales k) Finished Goods sold