Question

Table 1 below is an excerpt from the paper, Portfolio diversification with virtual currency: Evidence from bitcoin written by Guesmi, Saadi, Abid, and Ftiti and

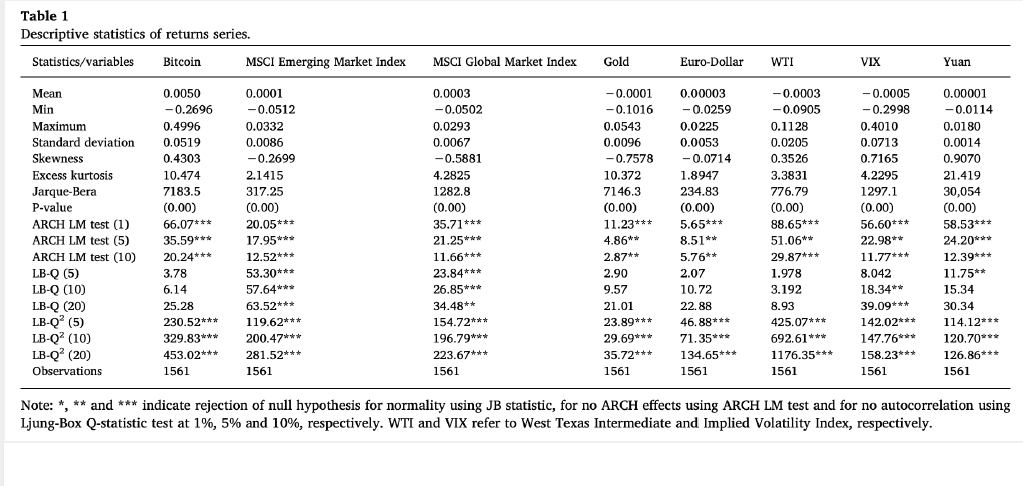

Table 1 below is an excerpt from the paper, "Portfolio diversification with virtual currency: Evidence from bitcoin" written by Guesmi, Saadi, Abid, and Ftiti and published in the International Review of Financial Analysis in 2019.

These time series are skewed to the left: ___

These time series are skewed to the right: __

These time series are platykurtic: __

These times series are leptokurtic: _____

Then, use the information on skewness and excess kurtosis and write one or two sentences explaining whether the bitcoin or WTI (crude oil) time series is riskier for the time period used in the study.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exercises In Computational Mathematics With MATLAB

Authors: Tom Lyche, Jean Louis Merrien

1st Edition

366243511X, 9783662435113