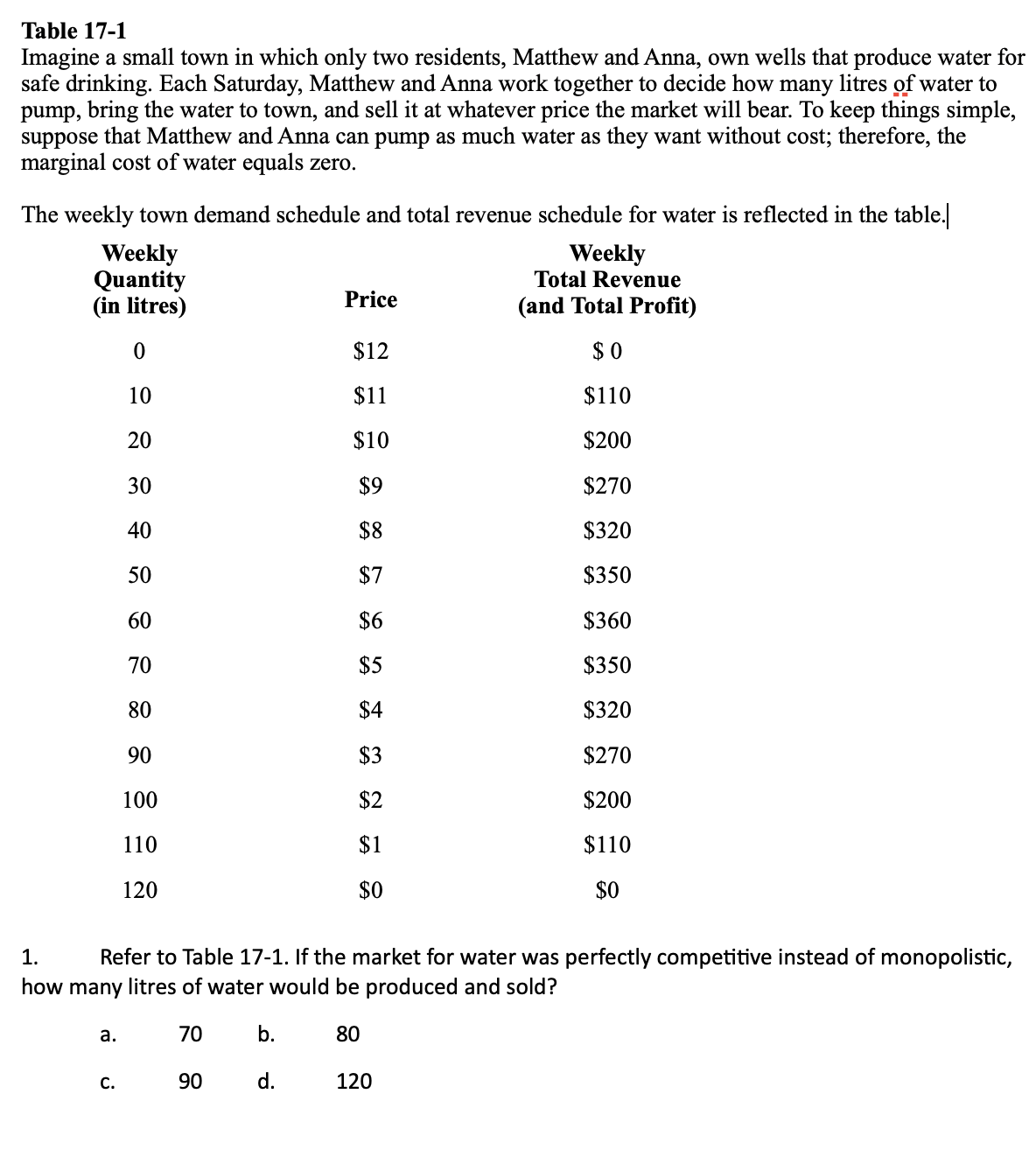

Table 17-1 Imagine a small town in which only two residents, Matthew and Anna, own wells that produce water for safe drinking. Each Saturday, Matthew

Table 17-1 Imagine a small town in which only two residents, Matthew and Anna, own wells that produce water for safe drinking. Each Saturday, Matthew and Anna work together to decide how many litres p_f water to pump, bring the water to town, and sell it at whatever price the market will bear. To keep things simple, suppose that Matthew and Anna can pump as much water as they want without cost; therefore, the marginal cost of water equals zero. The weekly town demand schedule and total revenue schedule for water is reected in the table.| Weekly Weekly Quantity Total Revenue (in litres) Price (and Total Prot) 0 $12 $ 0 10 $11 $110 20 $10 $200 30 $9 $270 40 $8 $320 50 $7 $350 60 $6 $360 70 $5 $350 80 $4 $320 90 $3 $270 100 $2 $200 110 $1 $110 120 $0 $0 1. Refer to Table 17-1. If the market for water was perfectly competitive instead of monopolistic, how many litres of water would be produced and sold? a. 70 b. 80 c. 90 d. 120 2. Suppose a perfectly competitive market is taken over by three or four rms. What result would we expect regarding market output and the price of the product? a. an increase in market output and an increase in the price of the product b. an increase in market output and a decrease in the price of the product c. a decrease in market output and an increase in the price of the product d. a decrease in market output and a decrease in the price of the product 3. As the number ofrms in an oligopolistic market grows larger, what does the price approach? a. average total cost b. marginal cost c. marginal revenue d. the monopoly price 4. How do equilibrium prices in markets characterized by oligopoly compare with those in monopolies and perfectly competitive markets? a. They are higher than in monopoly markets and higher than in perfectly competitive markets. b. They are higher than in monopoly markets and lower than in perfectly competitive markets. c. They are lower than in monopoly markets and higher than in perfectly competitive markets. d. They are lower than in monopoly markets and lower than in perfectly competitive markets. 5. If dupnpjists individually pursue their own selfinterest when deciding how much to produce, what do we know about the price they are able to charge for their product? a. It will be less than the monopoly price. b. It will be equal to the monopoly price. c. It will be less than the perfectly competitive market price. d. It will be equal to the perfectly competitive market price. 6. As the number of rms in an oligopoly grows larger, what does an oligopolistic market look more and more like? a. a competitive market b. a monopoly c. a duopoly d. a monopolistically competitive market 7. Assuming that oligopolists do not have the opportunity to collude, once they have reached the Nash equilibrium, what actions will they take next? a. It is generally in their best interest to raise the price of the product. b. It is generally in their best interest to supply less to the market. c. It is generally in their best interest to leave their quantities supplied unchanged. d. It is generally in their best interest to lower the price of the product. 8. Self-interest usually results in what kind of outcome for the players in a prisonersT dilemma game? a. optimal outcome for both b. less than optimal outcome for both c. dominant outcome d. cooperative outcome

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance