Answered step by step

Verified Expert Solution

Question

1 Approved Answer

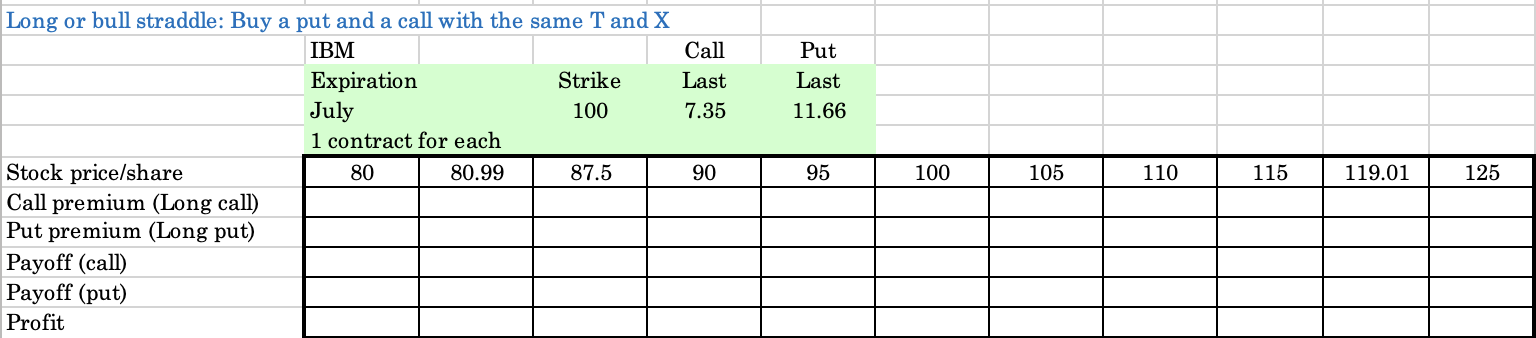

table [ [ { table [ [ Long or bull straddle: Buy a put and a call with the same T and X

table

tableLong or bull straddle: Buy a put and a call with the same T and XIBMExpiration,,Strike,Last,Last,,,,,,July,, contract for eachStock priceshareCall premium Long callPut premium Long putPayoff callPayoff putProfit Question Long or bull straddle: You longed a July put contract and a July call contract with the same strike price $ Please predict the profit of your portfolio based on possible future stock prices by completing the table.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of The Economics Of Finance Volume 2A

Authors: George M. Constantinides, Milton Harris, Rene M. Stulz

1st Edition

0444535942, 978-0444535948