Answered step by step

Verified Expert Solution

Question

1 Approved Answer

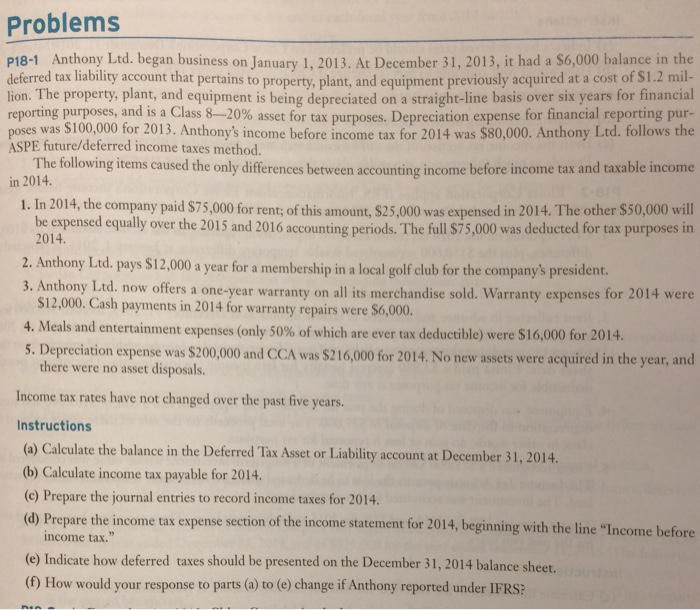

Taken from 'Intermediate Accounting' 10th Canadian edition Volume 2 by Kieso, Weygandt, Warfield, Young Problems P18-1 Anthony Ltd. began business on January 1, 2013. At

Taken from 'Intermediate Accounting' 10th Canadian edition Volume 2 by Kieso, Weygandt, Warfield, Young

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cima Official Exam Practice Kit Fundamentals Of Management Accounting Cima Certificate In Business Accounting 2006 Syllabus

Authors: Walter Allan

2nd Edition

0750687177, 978-0750687171